Apollo and what even is private credit?

The term “private credit” labors under the weight of negative connotations, yet remains poorly defined. A loan made by a BDC to a middle market widget manufacturer is considered private credit. That same loan made by Bank of America or JP Morgan is not. A loan made by a credit fund to a PE sponsor to finance the buyout of a widget manufacturer is private credit. That same loan made by a bank and broadly syndicated to investors is not. Why should the particulars of who makes a loan and how widely it is held – rather than the fundamental characteristics of the loan itself – be of such foremost importance as to merit an entirely distinct label and asset class?

Many investors think of “growth” and “value” as superfluous classifications that have no bearing on what we ultimately care about, which is the relationship between the stock price and the value of an enterprise. “Growth and value are two sides of the same coin”, as the saying goes. Likewise, whether a loan was originated by a bank or by a credit fund, what matters is whether it pays principal and interest according to schedule. Value is value. Credit is credit.

Marc Rowan put it like this recently:

The notion that a loan is somehow riskier because it wasn’t originated by a bank is not a coherent argument. Private credit is just credit. You underwrite it well and it performs. You underwrite it poorly and it doesn’t. If you are concentrated in one industry and you are seeking very high returns and you do things other than first lien, and you do things that are highly PIK and highly structured with smaller companies, you will suffer losses in pursuit of higher returns. If you run a large cap only, first lien only, cash pay only, less levered credit book on a fully diversified basis, you will not suffer losses absent a massive credit cycle, in which case credit everywhere in the economy will be affected. (Apollo Global Management, Inc., Q1 2026 Earnings Call, 5/6/26)

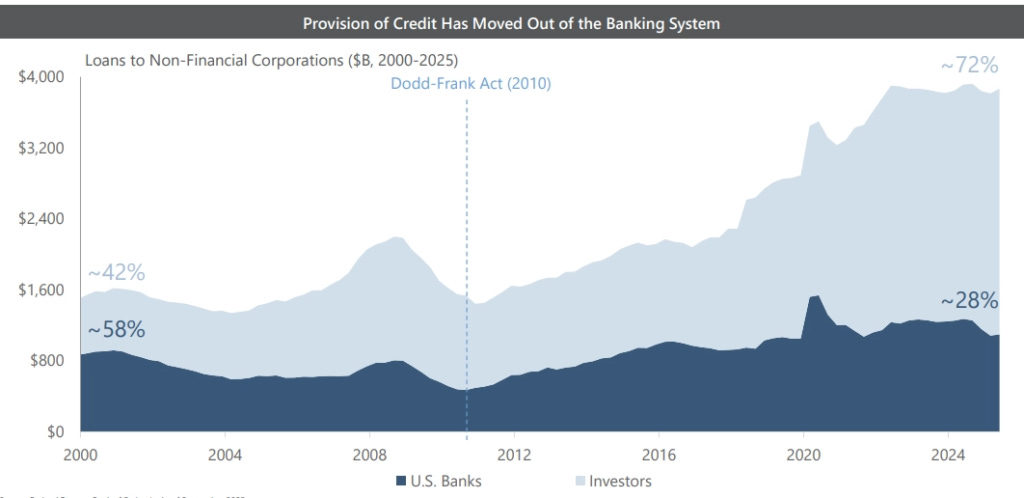

In the aftermath of the GFC, banks were hit with onerous capital requirements that constrained balance sheet capacity. Investors stepped in to fill that gap. Maybe the surge in non-bank credit, from ~$500bn in 2015 to ~$1.3tn in 2025 ($2tn, according to Apollo), is what has people on edge.

Source: Apollo