[FISV, GPN, FIS, SQ, Stripe, Adyen] On payment processors, distribution, and technology: Part 4 of 4

If you follow the payments space even casually, you are no doubt aware of the sequence of the mega mergers that have taken place between merchant acquirers and core processors this past year.

The bolded companies in the table above are the surviving merged entities, their market caps and enterprise values current through yesterday. Italicized are the constituent companies of the surviving entity. Their market caps and enterprise values are as of calendar year-end 2018, before any of these mergers were announced.

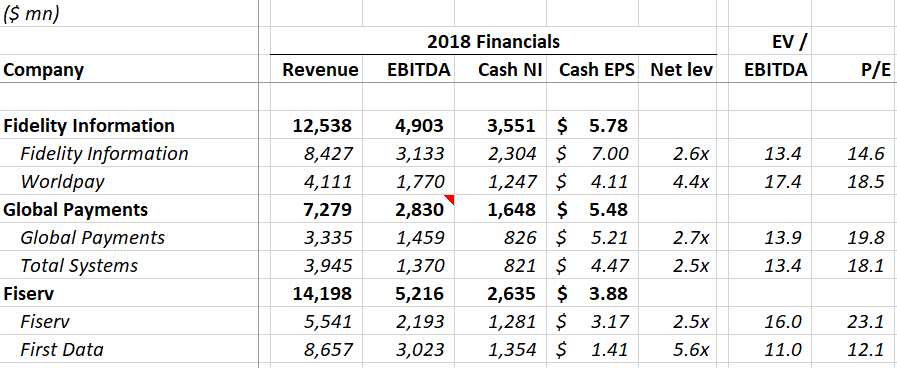

Here is a summary of their financials and trading multiples, as of year-end 2018:

As I scan the vast expanse now occupied by these new behemoths, I must pause to remind myself what it is I’m looking at. The new Fiserv is, on one side, a rollup of hundreds of companies (many of those companies roll-ups of other companies)…a morass of 700 products that spans account processing, card processing, payments, electronic billing, loan processing, and that target small banks, large banks, credit unions, as well as non-bank billers like insurance companies, utilities, and telecom providers; and, on the other, a mosh pit of merchant acquiring platforms that legacy First Data tried, but failed, to consolidate plus an issuer processing business plus a debit payment network. I can’t even begin to fathom the degree of infrastructure heterogeneity underpinning it all. It’s bewildering.