[LYV – Live Nation Entertainment] Some of It’s Magic, Some of It’s Tragic

Live Nation’s business model is unique, contextually rich, and complicated. While I think this is a decent business – to see this you have to consider all its parts, some of which are mediocre on a standalone basis, as an interlocking whole – I don’t think the purported “platform” is as interesting as I initially believed and others have claimed. I’ll start with a straightforward look at the various segments and reserve critiques until towards the end.

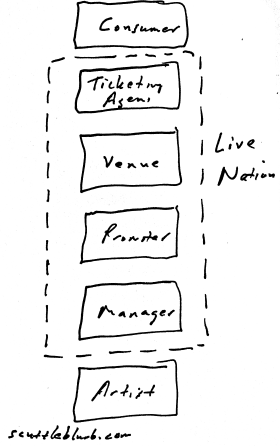

Here’s a high level view of the concert value chain. Live Nation participates in nearly all parts of it. Artists hire managers, who deal with promoters, who negotiate with venues, who choose the ticketing agent that ultimately sells tickets to the consumer:

You can see why nosebleed seats for Metallica’s concert this May in Baltimore will cost you over $90 all-in. It’s a long way from the artist to the consumer with a lot of money changing hands at every point. Recriminations about who exactly has been responsible for gouging consumers on ticket pricing over the years – the promoter pool? the ticketing monopoly? the artists? – have been flung up and down the stack.

The logic behind vertical integration is obvious: the various markups assessed by one part of the value chain is recaptured by another. In econ speak, vertical integration allows the consolidator to grab value by eliminating “double marginalization,” whereby two independent firms, one upstream and one downstream, each with market power, apply markups above their respective marginal costs. Merging and doing away with one of those markups removes at least part of the deadweight loss that results from pricing above marginal cost.

[I found the Ticket Mastersby Dean Budnick and Josh Baron helpful in understanding the historical backdrop of the concert and ticketing industry. If you are interested in this space, definitely read that book].

Artist Nation

In 2007/2008, back when it was a part of IAC, Ticketmaster beat out Live Nation in bidding for a controlling stake in Front Line Management – an artist management business run by the notorious Irving Azoff – which prompted Live Nation to start its own management company, Artist Nation, trumpeting its presence with a splashy 10-year $120mn deal with Madonna in October 2007. Other huge $50mn-$100mn purchases of artists’ rights – often partially paid in stock options – followed, including $50mn-$70mn for Nickelback. Nickelback! Needless to say, the market did not take kindly to these deals.

A manager negotiates on the artist’s behalf and collects a percentage of her earnings, usually under long-term agreements. On its own, AN is a sub-par business and because the personal relationship an artist has with her manager is important, doesn’t scale well at all. LYV management will often assume a defensive posture whenever questions around this segment are raised and almost never calls it out it independently on conference calls. Over the last 5 years, revenue has been flat while profits have declined dramatically. Conveniently, the company is now merging AN into the Concerts segment, so we won’t get separate disclosure for this segment in future quarters.

For labor (in LYV’s case, the artist managed by Artist Nation) to be a sustainable source of competitive advantage, it must create more value inside the company than it could elsewhere. I wrote about this concept 5 years ago in a bearish report on Digital Domain (DDMG):

“While management is quick to foreground the deep bench of talent it has recently acquired for Digital’s animation studio, including marquee names from Disney, the key question [from a value-accretion perspective] is whether these individuals, when paired with DDMG’s unique assets, create more value inside the Company than they could at Disney/Pixar or anywhere else. If not, it’s difficult to argue that these human assets are immobile, and thus a source of sustainable competitive advantage.”

Value must first be created before it can be shared between those creating it. So, does an artist create more value dealing with Live Nation than she could with another manager/promoter and how is that value divided? There are several relationships to consider.

The first is between the performer and Artist Nation. One could argue that contracting with Live Nation gives the performer access to LYV’s owned/contracted venues and considerable promotion muscle, while Live Nation earns ticket/concession/sponsorship revenue off the audience that the artist attracts. The problem, however, is that once the talent attains prominence, she is responsible for an increasing proportion of the surplus and in a position to claim more of it. Beyonce will sell out any venue, whether she is managed by Live Nation or not. She, not the manager, creates the value and has the leverage the take it.

While management maintains that AN shouldn’t be viewed in isolation, AN-represented artists played before less than 10% of Live Nation’s fans across just 2% of Live Nation’s total shows, so I’m not so sure this segment is as “paramountly strategic to our concert business” as the company avers. Also, the consent decree that Live Nation signed with the Justice Department in 2010 as part of its merger with Ticketmaster (TM), expressly prohibits Live Nation from wielding Artist Nation as leverage to force venues into employing TM as a ticketing agent (though, I’m sure there are subtle ways to circumvent this provision). At the end of this post, try to imagine Live Nation without Artist Nation. I think you’ll find that the core value drivers are unimpaired.

The second relationship, between artist and promoter/venue, is trickier. Unambiguously, Beyonce + 30k-seat Live Nation amphitheater creates more value in total (tickets, concession and parking, sponsorship) than Beyonce + Moosehead Bar and Lounge. But, who has the bargaining power to claim more of it? Is it the chart-topping artist with a huge following on whom the venue relies for sponsorship revenue or is it the venue (or group of venues in the case of a tour) on which the artist depends for her income? The scales still tilts in the artists’ favor here too as there are plenty of regional promoters competing for acts…this is an weird instance where more competition – in the form of promoters/venues competing for performances – actually results in higher prices to consumers. But relative to AN, there’s more value for Live Nation to claim in this segment.

Live Nation actually only owns 26 of its 196 venues; it leases (86), has exclusive booking rights to (61), operates (19), and has equity interests in (4) the rest. The leases are 10-20 years long, so LYV effectively has a lock on those. But outside of that, why do venues ink deals with Live Nation vs. another promoter?

This post from the @U2 blog, which lays out the details between the Meadowlands complex and Live Nation for 2 U2 concerts performed between 9/23 and 9/24 2009, is illuminating. Per the blog post (emphases mine):

Stadium rental fee: $252,500, plus $15,000 per day if additional time is needed

Ticketmaster is the approved ticketing agency.

All seating is reserved, floor is general admission.

Four ticket prices: $253, $98, $58 and $33

Stadium authority gets to set aside 750 tickets per show and buy them from Live Nation at discounts: $25 for $253 tickets and $15 for $98 and $53 tickets.

Stadium authority gets to collect and keep $15 service fee on $253 tickets, $10 service fee on $98 tickets and a $5 service fee on $58 tickets.

Ticket prices include $3 facility fee, to be split equally between stadium and Live Nation. Ticketmaster also entitled to charge a convenience fee.

Stadium gets to keep use of 9 suites at no charge.

Stadium can hold tickets related to obstructed view suites until Sept. 14 – after that date, all held seats will be released to general public for sale.

Live Nation gets 100 parking passes, plus parking space for working personnel.

Live Nation has a separate contract with Aramark for merchandise sales. Split is 77.5% / 22.5% on sales, which can change to 80/20 split based on sales totals.]

In addition to rental fees, the stadiums get paid part of the service fees assessed on ticket sales. This at least partially gets to the heart of why Ticketmaster, which purports to sell tickets more effectively than any other competitor, is important to the entire Live Nation enterprise and why any doubts I harbor about the future competitive standing of Ticketmaster infect, to some degree, Live Nation’s other businesses.

Which leads to the third, most critical relationship. The agreements that Ticketmaster (TM) have with venues indirectly, obliquely, and unquestionably represent the primary point of leverage that Live Nation (which owns Ticketmaster) has over performers. I’ll dig into this later in the post, but for now, know that Ticketmaster has an effective monopoly on primary ticket distribution domestically, which means that any artist who wants to perform at most marquee venues in the US must agree to have Ticketmaster exclusively distribute her public tickets. Of course, sometimes an artist is so popular that concessions on ticket allocations are granted and hippy jam bands like String Cheese and Grateful Dead have managed to squirm free of TM’s grasp; but for the most part, Ticketmaster has leveraged its dominant venue share to profitable effect for decades.

Concerts and Sponsorships

Way before Live Nation was Live Nation, it was SFX Entertainment, a concert venue roll-up founded in the late-90s by former radio/TV station consolidator Robert Sillerman that at its peak was the country’s largest promoter/venue operator, at one point responsible for 30% of Ticketmaster’s volume. SFX’s strategy was to acquire venues at egregious prices with the aim of knitting a massive, targeted advertising platform. Advertising and sponsorship were so central to the company’s future that it reputedly paid 5%-10% above an artist’s asking price to secure as many performances on as many venues as possible. In February 2000, 3 years into its journey – loaded with debt, bleeding cash, and still without any major ad contracts – SFX was acquired by Clear Channel for a stunning $4.4bn under the conceit that radio stations, billboards, and concert venues (SFX had 130 venues at the time and was the largest promoter in the country) would deliver natural promotion synergies (advertising artist performances on billboards, for instance) and a comprehensive, integrated medium for large advertisers. In an alternative history, one absent a bubble-era bid, SFX probably collapses under the weight of its debt burden just as Sillerman’s EDM roll-up would 16 years later. [The SFX acquisition was the second rabbit Sillerman pulled from his hat, the first being his sale of SFX Broadcasting to CapStar in 1997 for $2.1bn. For his third act, an electronic music roll-up that went bankrupt 4 years after IPO, he would draw a carcass]. But the synergies never fully materialized as hoped and public criticism over purportedly abusive monopolistic behavior mounted. At least part of the synergy issue was that the rolled-up regional promoters who viciously competed with one another in a prior life remained stubbornly wed to their old practices and mutual animosities, and developed fresh antipathy towards their new corporate overlord in many cases.