Class 1 freight rails: part 2 – freight types, route structures, and growth

Burlington Northern Santa Fe, Canadian National, Canadian Pacific Kansas City, CSX, Norfolk Southern, Union Pacific

Part 1 of this series offers a historical survey of how today’s Class 1 rails came to be. Parts 2 and 3 start at the ground level with the very basics of freight carriage, build up to an understanding of how an industry that had destroyed over most of its 200-year history managed to turn itself around, and conclude with some thoughts on investment implications.

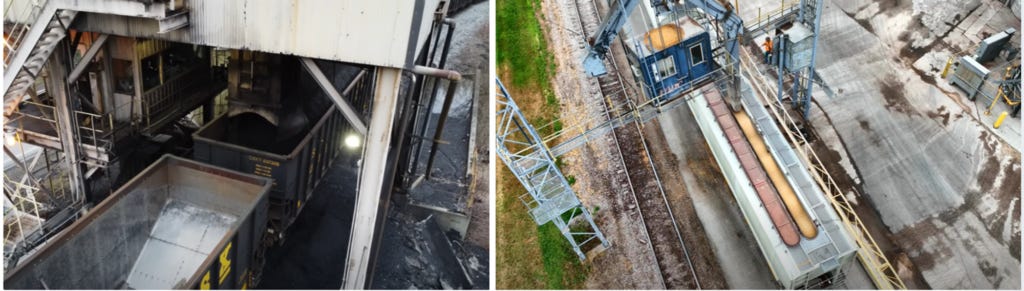

Different kinds of freight are transported in different ways and are profitable to different degrees. Huge volumes of bulk commodities are hauled in unit trains, long stretches of homogenous railcars, sometimes more than 100 long, ambling one by one under a chute that dumps grain or coal into each car, with all cars holding exactly the same commodity and heading directly to a common destination, like an industrial conveyor belt.

Unit trains are a recent phenomenon, arising in the mid-20th century so commodity producers could fill an entire train at once instead of renting individual cars piecemeal. Today, they account for about 70% of US grain moved by rail and 70% of coal shipped to power plants. They don’t deliver the highest revenue/unit but tend to be the most profitable because:

a) there is no viable alternative for transporting massive amounts of bulk commodities over long distances. A single railcar can carry 3x-4x as many tons as a single truckload (that is, you’d need about 400 trucks to replace the carrying capacity of a typical 100-car unit train)

b) shippers are often captive to the railroad whose tracks run through their grain elevator or coal processing plant; and

c) they travel directly to destination terminals without intermediate stops and move at lower speeds than intermodal and merchandise trains, thereby consuming less fuel per ton mile

Intermodal trains operate as part of a broader logistics system where containers are transferred between different transportation modes. In international intermodal, a container with furniture or appliances from China might be ferried overseas on containership to a port in Los Angeles, where it is hoisted alongside containers from other shippers onto an intermodal train that carries the aggregated haul to a terminal, where the container is put on a truck and driven to a fulfillment center. In the case of domestic intermodal, where containers are shipped from one distribution center to another, the first and last mile are carried by truck, the longer intermediate journey by train.

Besides its interaction with other transportation modes, intermodal differs from unit trains in several other ways:

First, they carry a wider range of goods, really anything that can be transported in standard shipping containers, including consumer products (electronics, appliances, clothing), building materials and equipment (plastics, spare parts, tractors, machines), and food and beverage products (coffee beans, beer).

Second, in many cases the intermodal carrier will interact with major intermediate logistics coordinators like JB Hunt (whose logo features prominently on the containers imaged above), Schneider, or Hub Group instead of directly with end customers

Third, the service is more service sensitive because end customers are often retailers or manufacturers who operate according to tight delivery windows

Intermodal trains tend to carry the lowest margins because they compete directly with speedier and more reliable truck service. In a logistics network, intermediate stops and touches introduce complexity, and complexity introduces more opportunity for errors. All else equal, you’d rather have a single truck haul a container from one warehouse door to another than have a truck deliver a container from an origin warehouse to an intermodal terminal and then have it transported by train to another terminal, where it is then picked up by another truck that completes the final mile.

With longer hauls in the West, Union Pacific and BNSF realize about twice as much revenue per intermodal carload than CSX and Norfolk Southern (~$1,400 vs. ~$700). Even so, from a shipper’s perspective, the cost to intermodal over distances greater than 1k miles is substantially cheaper than using truckload carriage from beginning to end, roughly 30%-40% for a cross-country haul compared to maybe 10%-15% on a 600-700 mile journey. Routes less than 200 miles, more common in the East where warehouses are closely clustered together, are subject to especially fierce competition from truckers.

Merchandise trains have long been the bread and butter of railroads. Unlike intermodal trains, they carry bulky, non-containerized goods like chemicals, steel coils, lumber, fertilizers, and automobiles. And unlike unit trains, they contain a variety of goods from different customers on cars that are switched at yards from one train to another based on common destinations. Merchandise trains fall somewhere between intermodal and unit in terms of tightness of scheduling windows and truck competition.

One should not take these categories too literally though, as railroads will pair freight to train type based on what’s best for the overall network than for any given haul. Unit trains are the most profitable but bulk commodities like coal and grain are sometimes intermingled with lumber and steel on merchandise trains to minimize train starts and balance crew and equipment. Intermodal and merchandise freight are also often co-mingled on the same train. Phosphate and aggregates are often moved on merchandise trains but at large enough quantities can also be shipped on unit trains.