[SERV – ServiceMaster; ROL – Rollins] Scale Economies and Hard Realities: Part 2

Countless termites die every day from natural causes, and that makes them the lucky ones. Many are poisoned by liquid pesticide sprayed along entry routes into homes. Still others are duped into ingesting toxic morsules that they share with nest mates, unwittingly wiping out whole colonies, slowly, over months. More creatively (and less commonly), they are frozen in liquid nitrogen, zapped with microwaves, burned alive, or gassed, their reepers, draped in Orkin red and white or drab Terminix khaki, devising ever more lethal ways to extinguish broad swaths of these and other ravenous nuisances – mosquitos, ants, bed bugs, cockroaches – that impose serious and trivial encumbrances on our daily lives. Plus, they’re gross to look at. Especially in commercial joints like restaurants and food processing facilities, where the “cost of failure” relative to treatment is unacceptably great. We have the prerequisites for predictable demand that is basically recession resilient…but does that translate into a good business?

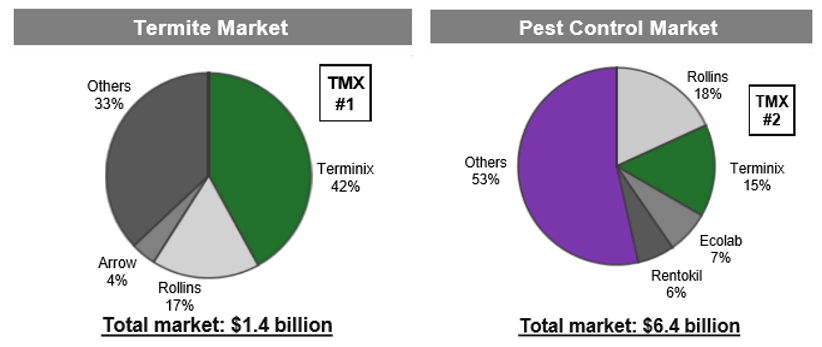

Much of what you need to know about competing in pest control is nicely captured in this tweet:

Ok, so you want to open a pest control branch. After getting a license from state’s Pest Control Board, registering your business, buying a used truck or van from the local dealer, procuring poison and poison dispensing equipment, and insuring yourself against public liability and property damage, you’re probably out $20k to $50k from the get go. No big deal. That’s why you’re in the mix with over 20,000 other pest control operators in the US. Now you need customers…but no one knows who you are. So you put up flyers, buy space in the yellow pages, and compete for key words against dozens, possibly up to a hundred, other pest killers in your service area, including the two big boys, Terminix and Rollins, who together already claim, say, 40% of your market and can outbid you all day long. And because you’re asking homeowners to let you onto their properties and in some cases, into their homes, awareness isn’t good enough. They have to trust you. Terminix (acquired by ServiceMaster in 1986) and Orkin (Rollins’ most well-known banner), have each burnished their brands and reputations over 90 years. Terminix holds the top spot for unaided and aided brand awareness in the industry and, thanks to Rollins’ 60 years of TV advertising, damn near everyone has an image of the immaculate Orkin man.

Source: ServiceMaster Investor Day (May 2016)

[Ecolab, which acquired its way into pest control in the mid-80s and now bundles it with cleaning and sanitation products, competes with Terminix and Rollins on the commercial side.]

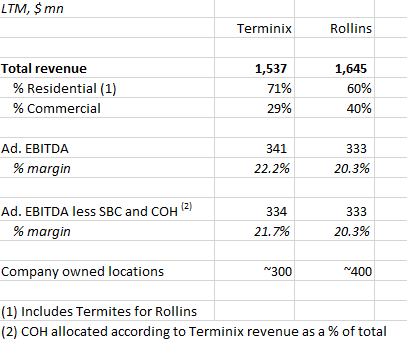

[Both Rollins and Terminix have some franchisees, but the vast majority of EBITDA for both companies comes from company-owned operations]

Having several times the market share of any other competitor in space means that whenever a Terminix or Rollins technician hits the road, he can make more stops per trip than competing technicians, each incremental stop along his route carrying negligible cost. Around 60c of every incremental revenue dollar drops down to profits that can be reinvested in brand marketing, advertising, training, and technology to attract still more customers and service them ever more productively. Through its Virtual Route Management, an advanced routing and scheduling system that has consumed a lot of investment over several years, Rollins now optimizes over 75% of its routes every day. This has cut technician driving miles by ~25%, bringing fuel and maintenance savings, improving speed-to-customer, and boosting the number of stops per mile [a Rollins technician does ~8-10 jobs per day]. And once got, as long as service standards are maintained, households are mostly theirs to lose, year after year, as the battle against pests and termites incessantly looms: 80%-85% of households renew their service every year [well above the industry retention rate of ~70%]; it’s more like 90% on the commercial side.

This process requires very little capex to maintain; over the last decade, over 60% of Rollin’s EBITDA has converted to free cash flow, around 20% of which has been plowed into tuck-in acquisitions at 5x-6x EBITDA, while it’s own multiple has steadily ascended from ~12x in 2009 to ~30x(!) today [although more recently, European pest control players Rentokil and Anticimex, have been aggressively rolling up US mom-and-pops at what both ServiceMaster and Ecolab have claimed are inflated prices, deflating returns on tuck-ins. The Europeans don’t appear to be behaving too uneconomically otherwise, but this situation bears monitoring]. When acquiring a mom-and-pop, Terminix and Rollins will typically shutter most of its branches, merge the acquired technicians into existing locations, drop their books of business onto existing routes, and cross-sell services (for instance, selling termite services to predominantly pest control accounts), precipitating more variable profits that are recycled into…you get the idea. This tune has been on repeat for Rollins and Terminix for decades.

So yea, pest control is a really good business…if you’re Rollins or Terminix. For nearly everyone else, it’s easy to get in but hard to grow.

Rollins and Terminix share the same core scale advantages but that doesn’t mean they have delivered comparable results. Compared to Rollins, which has grown its top-line organically by mid-single digits over the last 5 years, Terminix’ growth has languished. Changes in disclosure confound comparisons over time, but we know that retention rates for termite customers steadily deteriorated from 86.1% in 2011 to 84.5% in 2014 (still well above the industry retention rate of ~70%) and that the number of pest control and termite customers declined by low-single digits from 2012 to 2014. Organic growth rates recovered to 3% in 2015 before decelerating into 2016, flat-lining year-to-date, and flipping to negative in the most recent quarter, with particular weakness in the pest control business that comprises nearly 60% of segment revenue…and what little organic growth that has materialized over the last ~5 years has come from price hikes offsetting customer churn, hardly the stuff of sustainable value creation.

When comparing EBITDA margins of Terminix vs. those of Rollins, we see that Terminix margins have run several points better than Rollins for the last decade, even as both companies have delivered steady margin accretion over the years.

Much of this is likely mix related – Terminix has a higher concentration of termite and residential, which carry better respective gross margins than pest and commercial – but I’d bet that some of that discrepancy can be tied back to Terminix’s relative negligence reinvesting in systems and process. Over the last decade, Rollins has funneled ~10% of its EBITDA into capex vs. just 6% for Terminix, the latter’s capital spending taking a step down after being LBO’ed in July 2007 [by Clayton, Dubilier & Rice Inc. and others for 11x EBITDA. The company returned to the public markets in June 2014 massively levered (net debt / EBITDA of ~8x EBITDA in 2013, which has since been reduced to 3.5x through debt reduction and EBITDA growth). The private equity sponsors blew out of their shares in a series of secondaries in 2015 and do not own a significant stake in the company today.]

To get specific, in 2013 Rollins launched its Branch Operations Support System (BOSS) initiative, which:

1) placed BOSS-synced iPhones in the hands of its technicians, giving techs real-time scheduling updates and instant access to customer information, yielding easier cross-selling, better service, and ultimately stickier customers; and 2) platformed branches on a common operating system, giving upper management granular performance stats by branch and manage; and, as mentioned above, 3) introduced a new route management and scheduling system.