[VRSK] Verisk has standards

Upcoming posts (in no particular order): Gartner, Verisk, Visa/Mastercard, Tractor Supply, U-Haul, Apollo, Zoetis, and CCC (maybe)

In the mid-2000s, Verisk, faced with limited growth opportunities in an industry it had come to dominate, began placing bets beyond its core, confident that its experience building and managing datasets in one domain would carry over into others. It purchased a series of healthcare targets starting in 2004, then splashed into residential mortgages in 2008 through the acquisition of Interthinx, expanding that foothold with smaller add-ons that together formed the basis of a budding financial-services business, which would later include Argus ($425mn; 2012), a provider of credit card data that banks used for marketing purposes. Argus then crescendo’ed into the $2.8bn acquisition of Wood Mackenzie, a supplier of data and analytics to the energy and natural resources industries.

This all turned out exactly as well as you’d expect. The healthcare assets, a persistent drag on margins and growth, were divested in 2016. Argus’ high-teens organic growth decayed to low-single digits while its profitability collapsed. Wood Mac’s margins flatlined and growth atrophied in the midst of E&P headwinds. Verisk rid itself of these non-core, underperforming divisions, in no small part thanks to D.E. Shaw’s activist agitations.

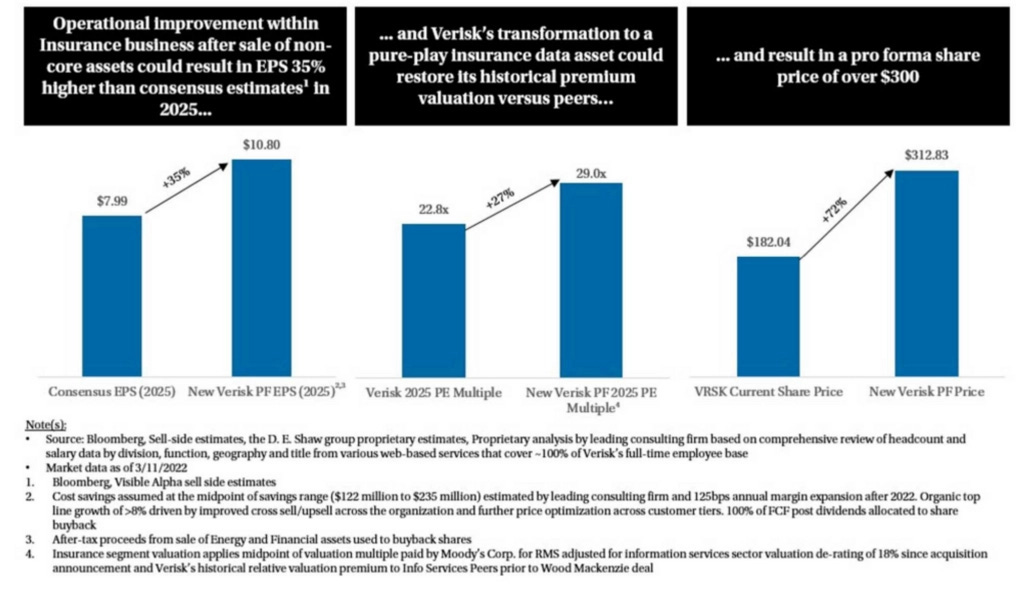

In its Value Creation Plan, D.E. Shaw laid out a plan for Verisk to grow EPS by 35% over the next 3 years, which, combined with multiple expansion (23x to 29x), would drive the share price 72% higher:

Well, 3 years have now passed. Last year’s EPS of $7.16 fell way short of Shaw’s $10.80 target (and of Consensus expectations too for that matter). The stock briefly kissed $313 on multiple expansion but has sold off over the past year on slower-than-expected organic growth and on, you guessed it, AI fears.

Before getting to that, it is worth briefly recapping what the slimmed down Verisk looks like today. It is now a pure-play insurance business, with roughly 60% of its portfolio tied to commercial lines, 40% to personal lines1. It gets around 70% of revenue from primary insurers, the balance from brokers, reinsurers, managing general agents (MGAs), and claims professionals. Around 80% to 85% of revenue is subscription-based, the other 20% to 25% scales with insurance premium growth. Most major clients are locked in through 3-year contracts with embedded price escalators.

Though it serves a cyclical industry, Verisk is bond-like in its consistency. With the sole exception of 2020, when it grew 5%, the company has organically grown revenue by 6% to 8% every year since its 2009 IPO. The cycle barely registers: revenue growth averaged 6.8% during soft markets, when underwriting capacity grows and pricing declines, and 7.3% during hard markets. Management expects more of the same, with 6% to 8% organic growth – split across pricing (3.5%-4.5%), cross/up-selling (1.5%-2%), and new products (1.5%-2%) – outpacing the insurance industry’s mid-single-digit growth over time. With 25bps to 75bps of annual margin expansion, EBITDA and EPS are expected to grow by 7%-10% and double-digits, respectively. A classic compounder profile.

What Verisk is best known for is aggregating detailed operational data from insurers and turning that data into standardized policy forms and loss benchmarks that are used as a starting point to build or update products. So rather than drafting every policy and pricing framework from scratch, an insurer can adjust Verisk’s templates and benchmarks to its own risk appetite and strategy. This core underwriting solution is surrounded by other datasets, including labor and material cost data for sizing the cost to rebuild a home or commercial property (360Value), and catastrophe models for gauging the probability and financial impact of wildfires, severe storms, and other extreme events in a given area (AIR).

In Verisk’s claims processing division, roughly half of revenue comes from insurers, the other half from third-party adjusters, contractors, and other ecosystem partners. Here, Verisk primarily offers two solutions.

The first, Xactware, which makes up the core of Property and Restoration Solutions (14% of total revenue, ~half of claims revenue), helps put on a number on physical damage and repair work. When a hailstorm damages a roof, a burst pipe floods a house, or a fire tears through a kitchen, insurers, adjusters, and often contractors turn to Xactware to estimate the materials and labor a repair will require and what it should cost.

The second, anti-fraud tools, comprising ~1/3 of Verisk’s claims-related revenue, are used to spot suspicious claims activity and detect fraud after a loss event. Verisk’s primary fraud fighting solution, ClaimSearch, is the world’s largest database of P&C claims information. Insurers comb through its 1.9bn+ records to uncover links across claims records and assess, for instance, whether someone has a history of filing lots of claims or whether their address or phone number has surfaced in other suspicious cases. Alongside ClaimSearch sit other anti-fraud tools, such as a digital media database of more than 600mn images – contributed in part by 5 of the top 10 carriers – that insurers use to evaluate suspicious claims photos (management cites research showing 30% of US consumers, and 55% of Gen Z respondents, consider it acceptable to manipulate submitted photos to maximize a payout).

These foundational datasets, undergirding Verisk’s underwriting and claims products, are complemented by workflow software and analytics that make use of it.

While many have excoriated Verisk’s misadventures in healthcare, financial services, and energy, its moat in insurance data and analytics has rarely come under question. Well, there was that brief flare-up in the mid-2010s, when some feared competitive encroachment by insurtech start-ups, a threat that ultimately proved toothless and passed without incident. But now investors are worried that AI could commoditize the job of gathering data and synthesizing it into usable insight, rendering Verisk’s moat obsolete. S&P, Moody’s, and other vendors of data and analytics have also sold off on this fear.