[ZO1 – Zooplus] Competing with Amazon

The demand side of this story is easy. As a former dog owner, I can assure you that there is nothing “experiential” about driving to Safeway and lugging 30lb bags of kibble back to the parking lot. Having it delivered to your front door is obviously the way to go. The supply side is more contentious and, as is the case for a growing number of industries, prominently features Amazon. Commentators are quick to reference addressable market size when prognosticating which product category will be next to fold to Amazon, but at least as important is the way in which the product is consumed. An ideally Amazonable product is one that is consumed in predictable fashion on a vast scale. Used cars are a large $740bn market in the US, but it is difficult to foster customer loyalty around a buying experience that takes place only once every 5 years, and decades hence, the notion that vehicle purchases will remain stable – in light of sexy trends like transportation-as-a-service and autonomous vehicles – is far from obvious. The US grocery market is also massive at $640bn, but the demand for groceries is highly predictable and the category offers a crucial entry point into the household.

What makes Amazon so fearsome a competitor to any e-commerce player focused on a single, frequently consumed product vertical is that it can be perfectly rational for Amazon to undercut and loss lead in any single category if doing so drives Prime subscriptions, intensifies spending in other areas, and reduces churn (as customer lifetime value scales non-linearly with retention). Pet food sales in the US, at “just” $80bn, is small compared to groceries…but, like humans, dogs and cats will be eating the same stuff in mostly the same way 20 years from now. They will eat it in vast quantity. Even if profits in this category remain scarce, Amazon probably won’t relinquish it because pet food largely piggy backs on the logistics infrastructure it already has in place and reinforces the set of goods that regularly touch households.

Consider Amazon’s brutal pursuit of Quidsi (diapers.com), which grew to $300mn in revenue before Amazon ruthlessly underpriced the poor company at every turn, going so far as launching the grossly unprofitable Amazon Mom program and losing $100mn over 3 months before Quidsi eventually kowtowed in submission and agreed to be acquired in late 2010 [the events leading up to the Quidsi acquisition are recounted in Brad Stone’s book The Everything Store] [In March 2017, Amazon announced that it was shutting down Quidsi and its various domains – wag.com, diapers.com, soap.com, casa.com, yoyo.com, beautybar.com – but obviously, the company hasn’t stopped selling pet food, diapers, personal care products, home decor, and cosmetics. It is just doing so under a single banner, Amazon.com].

I am not arguing that “profits don’t matter” for Amazon. I’m saying that what matters is optimizing profit dollars over the lifetime of a customer. And within that framework, I’m saying that profits are easy. Amidst a cornucopia of choice, customer loyalty is the scarce resource. In some respects, this is a tired claim. In past generations, habituation was got by nurturing brands that reduced the time and effort spent identifying quality, and those brands were reinforced by prime placement on the shelves of retailers. But the internet has changed all that: inventory is no longer space constrained, new products and services are far more easily discoverable and accessible, quality is more easily determinable, word-of-mouth and targeted advertising have allowed start ups to compete effectively against established incumbents. [For more on the topic of brand decay, check out Sean Stannard-Stockton’s excellent two-part post, The Death of (Many) Brands, Part 1, Part 2]

In one sense, it has never been easier to get discovered; in another, with the tools of the internet available to all, it has never been harder to stand out. But this leveling effect is backwards compatible and thrusts under fresh and constant scrutiny, mediocre products that have long taken refuge behind exceptional brands. Brands still matter, but they are less and less taken for granted. And in mass market especially, brand value is increasingly migrating downstream away from product and toward the customer interface, claimed by those who can best meet the twin demands of low price and convenience. Of course, here I am talking about Amazon, the company whom 45% of customers would trust as their primary checking account provider.

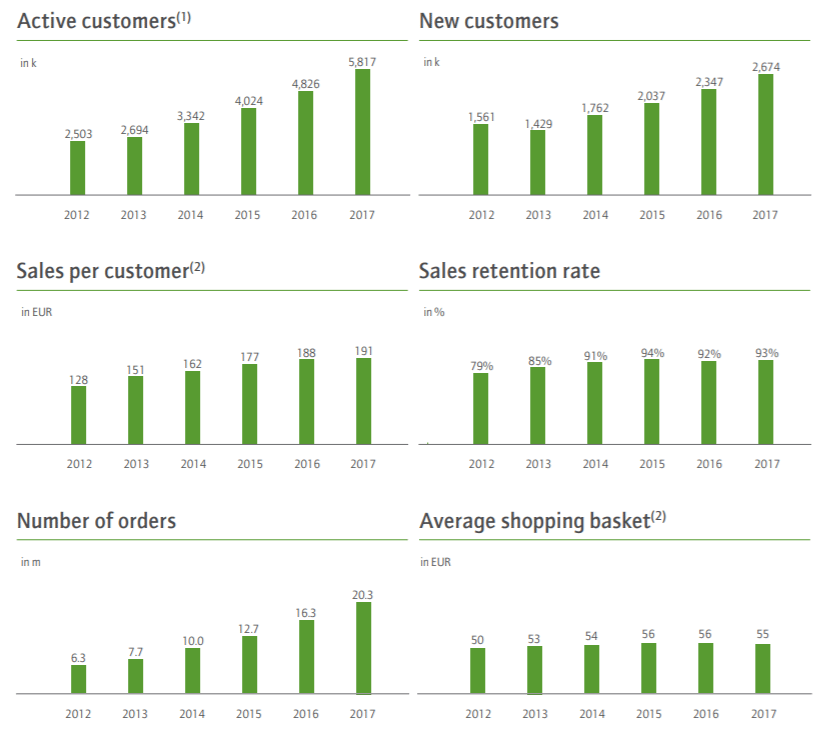

But as insuperable as Amazon’s advantages may appear, and despite competing in the pet supplies category for 12 years, Amazon is not the dominant e-commerce retailer in European pet food and supplies. That distinction goes to Zooplus, which claims ~40%-50% share of the online category vs. ~20%-30%(?) for Amazon. Amazon entered the category in 2005 and still, over the last decade, Zooplus’s revenue has ballooned at a 36% CAGR, from €53mn to €1.1bn, and gross profit dollars have grown by over 30% annually. It has generated positive cumulative EBIT profits and operating cash flows over this time. Here are the obligatory charts of impressive KPI trends:

Zooplus skeptics citing Amazon concerns have to contend with this reality.

Of course, Zooplus has its fair share of rabid bulls too. I haven’t joined that crowd yet because I don’t have a good gauge of what the structural profits of this business look like in light of, yes, persistent competition from Amazon….which is another way of saying that I’m not quite convinced that reinvesting in growth today will translate into big profits tomorrow.

Profits now or profits later? There are trade-offs to both perspectives. You can choose to hold margins by staying disciplined on price, but in a highly price sensitive market like pet food retailing, you will lose the future profits of defecting customers who find better deals elsewhere and lose operating leverage on your substantial fixed costs. Replacing that customer will require more marketing spend, nullifying the benefits of firm pricing. On the flip side, you can forsake profits and reduce customer churn by staying competitive on price, bolstering logistics, and ramping customer service, but today’s estimated lifetime customer values are hardly a given even then. If retaining customers means that you must engage Amazon in a ceaseless, brutal battle over price and service, you may never realize adequate profits to justify that investment…you may be running just to stand still.

But what we can say with a high degree of confidence is that abstaining from price competition and skimping on logistics for the sake of percentage margins is a losing strategy. Those margins will evaporate almost as soon as you show them because pet food shoppers are highly price sensitive, and there is a clear inverse relationship between delivery speed and churn rates, so lost volumes will translate into operating de-leverage. The only rational move, even if success is hardly guaranteed, is to focus maniacally on the “customer experience”…or, to put it less euphemistically, cut prices and invest in logistics. And that’s what Zooplus has done. The company has effectively retained existing customers, attracted new ones, and grown sales and orders per account, leveraging operating costs to such a degree that the heavy gross margin hits it has had to endure to stay price competitive, have been mostly offset over the last 10 years:

[When you include “other income”, Zooplus’ gross profits basically cover opex, netting to ~breakeven pre-tax profits.]

In at least one bullish Zooplus investment presentation, the author suggests that merchandise on Zooplus is systematically cheaper than it is on Amazon. My own work did not validate his findings. In early April 2018, I perused the German, UK, and French versions of Zooplus and Amazon websites and compared product pricing on more than a dozen randomly selected dog and cat SKUs, dry food and wet food. I was diligent about ensuring like-for-like package size comparisons [this can trip you up if you’re not careful because different sized packages yield different euros or GBPs per kilo]. I found that pricing on Amazon Prime and Zooplus was nearly identical in every case. While Zooplus did compare favorably on price – and at times, by a significant margin – against Amazon’s 3rd party sellers, I can’t say I discerned a hard trend. There are any number of intellectually honest sampling methodologies to choose from (I basically just threw a dart, but made sure to alternate which site received the dart and which site was cross-referenced) and, who knows, maybe Amazon realized they were behind the pricing ball and recently played catch up.

If you’re a bull, the main reason to play up this point about Zooplus’ supposedly lower prices is because you are presumably trying to suggest that Zooplus has a structural cost advantage to Amazon, right? For instance, the bull case for Ryanair is not that it has lower ticket prices than its competitors, but rather that its relatively lower costs enable it to price to levels that competitors cannot rationally match. By comparing the expenses across competitive carriers, we can plainly see that this is so, and we can also explain why:

“Like Southwest, Ryanair standardized on Boeing planes, targeted secondary airports, and operated with unforgiving efficiency all around. The operating model’s attendant cost advantages over incumbents, whose balance sheets were larded with legacy liabilities and whose cultures were poisoned with complacency, was recycled into lower fares, which lured growing waves of passenger traffic that were used to negotiate ever favorable landing fees at airports and volume discounts on Boeing aircraft orders. And those cost savings were plowed back into lower passenger fares, bringing still more traffic and so on. Legacy carriers, who must spend 3x-5x as much as Ryanair to carry a passenger, don’t stand a chance and engaging in a fare ware with Ryanair is path to sure ruin.”

So, everyday low prices is not itself a moat; it is a plausible proxy for cost advantage. Except, in the context of Zooplus vs. Amazon, is it? We don’t have the disclosure to really say….and what are we trying to say, exactly? Even if we could convincingly demonstrate that Amazon’s fulfillment infrastructure was ill-suited to handling the bulky heft of dog food; that Amazon’s 31 in-house operated fulfillment centers in Europe does little, relative to Zooplus’ 7 outsourced ones, to hasten delivery times or lower unit costs; that Amazon’s scale in manifold product categories doesn’t yield meaningful last mile unit cost advantages or scale economies on common fulfillment infrastructure; that Amazon’s dozen other points of contact with the consumer – from video to books to housewares – doesn’t translate into customer acquisition cost advantages in many other adjacencies; that customer support, including phone-based support, doesn’t unduly encumber zoolplus with relatively higher costs, we still have to deal with the fact that Amazon, like Zooplus, is also maximizing for customer lifetime value…except Amazon is doing so on much higher plane: it is not just trying to extract the most pet food dollars over a pet owner’s life, but everyday consumption dollars in a human life, period.

Zooplus can rationally lose money on the first year of customer acquisition under the premise that it will make many times its spend in future years; but Amazon can rationally price close to breakeven on a niche like dog food assuming spillover benefits of scale and customer acquisition and retention to other massive complementary categories. Trying to determine whether or not Amazon is making money in any single product sleeve is largely a fool’s errand and it’s the wrong frame besides, as Amazon is not evaluating the profitability of product categories individually but rather looking at the lifetime profit extraction opportunity on a bundle of goods and services holistically. Moreover, it seems to me that Amazon can take a “trust us” attitude with its shareholders to a degree that Zooplus cannot. Zooplus is not incurring deep losses to grow faster because its shareholders are closely tracking inflections in profitability. In September of last year, when Zooplus reduced full year profit guidance from a tight range of €17mn-€22mn to a “single-digit million amount” – that’s a ~€15mn hit on a sales base of €1.1bn – its shares lost 15% of their value within days. Amazon can get away with giving token guidance that is so wide – they expected somewhere between $300mn to $1bn in operating profits last quarter – as to be essentially meaningless.

The flaw in that argument is it assumes the only way to win big in this category is to beat Amazon on price and convenience. And yes, I think that when shopping for pet supplies, those dimensions are damn important; but they aren’t everything, and I actually think that the growing phalanx of Zooplus enthusiasts purporting that niche players can “beat” Amazon at its own game may be doing their stock pitches a disservice. Strategy is about trade-offs and I think the key here is finding a point of differentiation that Amazon, because of the very things that make it excellent at what it does, cannot replicate. Offering personalized and compassionate customer care and an online user experience catering to that need, for instance, is orthogonal to the one-size-fits-all approach that Amazon applies across all its product categories.

So, take Chewy.com, a US online pet retailer founded in 2011 that grew from $26mn in revenue its first year to “nearly $2bn” in 2017. By the time it was acquired by bricks-and-mortar competitor PetSmart for $3.4bn (or 1.7x revenue compared to Zooplus’ current valuation of 1x), it claimed 40% of the online pet food market compared to just 24% for Amazon. Chewy is staffed by pet lovers who are encouraged to bring their pets into work. They answer phone calls in seconds (I just tested this before typing that sentence and sure enough, someone – yes, a human being – picked up before the second ring. Nice!) and establish personal rapport with their customers through product knowledge. They take thoughtful, cutesy measures like sending cards on customers’ pets’ birthdays or flowers when a dog passes away. Chewy’s now parent, PetSmart, runs in-store and online adoption programs that have placed over 7mn pets in homes. Relative to rummaging through Amazon’s local sites, I found navigating Zooplus to be a far more pleasant experience. The latter’s site was populated with more detailed product descriptions, a side menu breaking down selection by brand, and even a prominently displayed customer support phone number at the top of the screen. [From what I can tell, customer reviews for both Zooplus and Chewy are excellent, though the Glassdoor employee reviews at both companies are somewhat wanting].

If merchandise were consistently offered at an identical price through a more user friendly web interface, would you opt to shop for the pet you love on Zooplus over an austere Everything Store with no heart in the pet category? Would you do so even if the former is somewhat less expeditious with deliveries? Is there a separate compartment in a pet lover’s consciousness and wallet, segregated from groceries and other human household items, reserved for pet-related nourishment and care and an affinity for retailers who share that concern? This gets a little soft and speculative, but I can buy into these premises. I’m not saying that you can win on flowers and cards alone. I don’t think Amazon will release its grasp on this category and along with Chewy, it too has been killing it in US pet supplies. According to One Click Retail, Amazon’s US pet product sales were $2bn (in a $40bn+ market, $30bn of which is food) after growing around 30% last year.

And as for Chewy, well, admittedly we don’t ultimately know how it would have fared as an independent company. At the time of its acquisition, Chewy was unprofitable and required regular capital infusions summing to over $450mn, with $200mn of that coming in its final years as it embarked on a capex heavy plan to in-house logistics. But still, by remaining within a tight range of Amazon with respect to price and convenience and animating the buying experience with personalized niceties that Amazon is constitutionally incapable of offering, perhaps a niche player can thrive alongside the Death Star.

And this brings us to the paint-by-numbers bull case. Pet supplies in Europe is a €23bn market. Zooplus, even with its 50% share of the e-commerce channel, has just 3%-4% of the total. In other words, it’s early and there’s plenty of room for more than one player to succeed. Zooplus has a clear and sustainable cost advantage relative to the brick and mortar players who are burdened with store leasing and staffing expenses. Stores still account for over 90% of the market but will almost certainly be donating share to both Amazon and Zooplus for the foreseeable future. [Share shift from physical stores to e-commerce is not a point of contention so I’m not going to belabor it, but just for your reference here is how Zooplus management compares its costs – the ones below the gross profit line like logistics, marketing, staff – to those of its B&M peers.

Pricing merchandise to Zooplus’ 24% product gross margins is clearly not a sustainable move if your operating costs run 40%+ of revenue. Granted, these B&M retailers derive a much greater mix of their business from higher-margin private label products – 40% of merchandise sales for UK-based Pets at Home and German pet retailer Fressnapf vs. just 11% for Zooplus, but the basic point still holds]

If you extrapolate revenue growth by 20%/year for 7 years, you get €4.2bn in revenue (assuming the broader pet supplies market grows by ~4%/year, €4.2bn in revenue implies ~13% market share). Assuming 5% pre-tax margins, nominal cash build, and 20x multiple on pre-tax profits yields an equity value over €4bn, implying a 20% annual return on the stock. Another angle is to consider that the current customer base is expected to generate €4.5bn in cumulative revenue over the next 5 years – the company is confident enough in this claim to refer to these sales as “locked-in” – yielding ~€450mn in incremental profits assuming a 10% contribution margin, which profits a true believer may assert will be reinvested at rates exceeding Zooplus’ cost of capital…clearly significant sums against today’s enterprise value of €1bn.

The unit economics today are compelling, underpinned by impressive customer retention: 93% revenue retention rate, 90%+ rrr’s in all 9 European countries in which it operates, and 3/4 of total sales coming from repeat customers acquired the year before. The annual survival rate of an account starts off at 79% after the first year but gradually climbs to around 95%-96% in years 6 and beyond, such that for the 2017 cohort, over the subsequent 10 years, a customer that costs €20 to acquire [that’s traffic acquisition costs per new account that shows repurchasing activity] is expected to bring in ~€1,730 in revenue and, assuming a 9.5% contribution margin, €164 of cumulative contribution profits [net sales minus all variable costs]. At any reasonable discount rate, the LTV:CAC ratio is enormous. The standard objections to fast growing tech/e-commerce companies – “Amazon doesn’t make money” and such – are now widely acknowledged as myopic ones that ignore reinvestment returns.

But it’s worth considering the pitfalls of the rebuttal too. In light of the continued ascent of fast-growing, profit depleting enterprises, it sometimes feels to me like we’ve swung closer to the other side of credulity, where investors seem willing (almost eager) to presume that any action that furthers the mission of customer experience will ultimately prove worthwhile to shareholders, and that current LTV/CAC ratios are sacrosanct and static. But of course, they are just estimates like anything else. The year before, Zooplus’ estimated 10-year sum of contribution profits from the 2016 cohort was €172 and the cost to acquire a customer was €15. Pre-tax losses on new customers has deteriorated from -2% of new customer revenue to -6%, as have the margins on existing customers, from +4% to +3%. Contribution margins have declined from 11% 5 years ago to around 9%-9.5% today. In other words, it has gotten more expensive to acquire new customers and keeping existing ones has meant meeting competitors on price.

That is why LTV, as impressive as it is against CAC today, still seems tenuous a concept in this price sensitive retail category. With enterprise software, you can have a high degree of confidence in the profits and average life of an acquired cohort because of significant switching costs. If you’ve got SAP installed, even if a competing vendor comes along selling a product with somewhat better specs and lower prices next year, you’re not going to rip and replace this key system of record for your company. SAP may lose the next engagement to a competitor, but its existing customer base isn’t going anywhere. Zooplus has no comparably compelling sources of customer captivity. It is not just the LTVs of incremental cohorts that are influenced by price competition, but all the existing ones as well. Imagine if Amazon shaved 10% off all their pet supply SKUs and Zooplus just stood back and did nothing. Its revenue retention rates would plummet across cohorts. Or, if Zooplus met Amazon’s price immediately, lifetime contribution profits would take a hit (assuming the price cut sticks across all future periods). Furthermore, revenue growth has decelerated significantly over the years…

…and simply extrapolating today’s growth out for the next 7 years may prove too ambitious. Now, this ain’t no Pets.com. The the background conditions 20 years ago were different: back then, there was greater dependence on expensive and less reliable analog brand media, relatively lower household internet penetration (only 1/3 of American households had access at the time), 100 other online pet supplies e-tailers swimming in a sea of easy money, and consumer trust issues transacting through a novel medium. And against those relatively impoverished and untested starting conditions, Pets.com spent an unspeakable $400/customer on marketing – including a $1mn+ Super Bowl commercial – at a time when Americans were spending less than $90 per year on their pets.

Zooplus, on the other hand, has generated profits even as it has grown its revenue by 35%+ per year over the last decade. Given mounting regulatory scrutiny, I don’t think Amazon’s going to pull a Quidsi, especially in Europe, where antitrust laws are concerned with protecting competition and not just impeding probable consumer harm, as is true in the US. But I can see a scenario where both Amazon and Zooplus both continue growing side-by-side, claiming B&M share, kicking ass, but where along the way, Amazon and other B&M retailers – which latter are losing traffic and have the margin to continue cutting prices in order to stay competitive – keep Zooplus huffing away on a pricing and logistics treadmill that keeps mid/high-single digit margins ever out of reach, creating surplus for Zooplus’ customers at the expense of its shareholders.

Strategically, it seems the way around this is to: 1/ force a wedge between your own products and those available on Amazon. Zooplus offers a panoply of wet and dry private label food brands for dogs and cats that collectively comprise 11% of sales. Not low-end versions of branded product…the good shit. Incidentally, premium pet food brands are a hot category right now (“humanization of pets”) and branded consumer food companies desperate for growth have been eagerly buying their way into this space. Recently, JM Smucker announced it would be acquiring Ainsworth Pet Nutrition, best known for its ultra-premium brand Rachel Ray Nutrish, for $1.9bn (2.4x sales). Before that, General Mills paid $8bn for high-end pet food manufacturer Buffalo Pet Products (22x synergized EBITDA). Zooplus’ private label brands are growing at nearly twice the rate (~40% y/y) of its overall sales and claiming greater than twice the wallet share of repeat orders compared to first time orders.

One possible concern here is that offering proprietary private label products may compromise the relationship Zooplus has with established third party brands. But as I mentioned earlier, specialist offline pet retailers, who account for over 90% of the market, derive a much greater proportion of their sales from private label compared to Zooplus. Besides, established brands looking for growth don’t really have much of a choice…where else are they going to find double digit sales growth? In the US, Blue Buffalo’s sales to national pet superstores declined in 2017 while sales to e-commerce channels grew by over 75%. And as private label mix continues to grow, so too should profitability (all else equal of course). Zooplus gets around a 10% gross margin lift from private label vs. established brands. Most of this probably gets soaked up by incremental brand marketing costs – Blue Buffalo spends around 10% of sales on advertising; I doubt it’s quite as high at Zooplus – but on such a low margin business, every point counts.

and

2/ re-orient the bundle.

I’ve spent much of this post fretting over Amazon because pet food comprises nearly 85% of Zooplus’ sales and I see pet food as a natural complement to human consumables…you pick up a bag of dog food as you shop for groceries. In the US, over half of pet food is sold through the Food-Drug-Mass channel. In Europe, it’s more like 60%. But hey, that still leaves 40% of the market, or $10bn, that goes through specialists, shopped at by those looking for premium SKUs, broader assortments, and other pet services that you won’t find at a supermarket. Zooplus can bundle food with other pet-related services – matching pet owners with vets, groomers, or pet insurers, fostering a consumer marketplace for dog sitting and walking services…who knows! – and capture this demo. It has nearly 6mn active customers, the vast majority of whom stick around from one year to the next. This seems like a good foundation off which to build a “go-to” venue for a slew of pet needs, food and otherwise. The company is experimenting with some of this stuff now, and even if these ancillary services don’t monetize, they can at least serve as customer retention tools.