[ZTS] Zoetis could use a booster shot

MBI and I recorded an episode of Never Sell recently (Scuttleslops, OpenAI valuation, Ryan Specialty) (Spotify, YouTube)

Upcoming posts (in no particular order): Gartner, Visa/Mastercard, Tractor Supply, U-Haul, CCC, and OTC Markets

Zoetis is the former animal health division of Pfizer, with roots reaching back to the 1950s. In the years following its 2013 spin-off, it introduced a number of therapies for dogs and cats that went on to become blockbusters in the pet world:

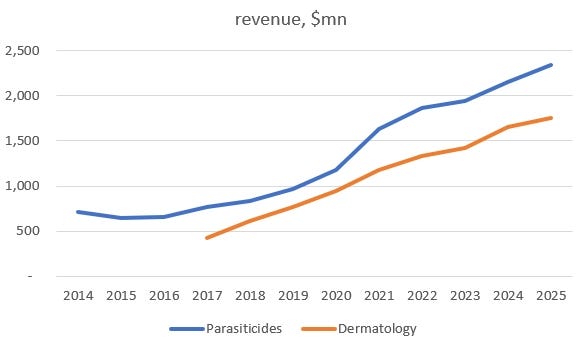

Simparica and Apoquel are $1bn+ franchises that made up 16% and 12% of Zoetis’ revenue last year, respectively. Together, they’ve been responsible for ~54% of Zoetis’ incremental top-line growth since 2013. Last year, Cytopoint, the pet health market’s first monoclonal antibody, did around ~$650mn while Librela likely contributed more than ~$500mn. Those four products sum to just under 90% of the total revenue that Zoetis reported in 2012.

Back then, the company got ~65% revenue developing and selling medicines and vaccines for livestock (cattle, swine, poultry, sheep, and fish). But with Zoetis’ Companion Animal (pets) segment averaging low-teens growth over the next decade as Livestocks’ languished at a low-single digit pace, revenue mix has completely flipped:

This shift from livestock to pets was rightly celebrated. Livestock drugs are far more of a commodity. The large producers who typically buy them are concerned, first and foremost, with cost effective protein production and procure treatment for hundreds or thousands of heads. Moreover, cattle and pigs are slaughtered after a few months or years and therefore, aren’t treated for chronic conditions. Livestock drugs rarely grow to $1bn franchises and those that do are swiftly decimated by generic versions come to market.

Pets are completely different. We love our dogs and cats, and care for them over 10 to 15 years. The choices we make regarding their welfare are motivated at least as much by emotion as by cold, economic calculus. We tend to stick to medications that our pets tolerate and only reluctantly experiment with similar and even cheaper, drugs. We’ll stretch our wallets for a chewable version of a drug because we feel bad about forcing pills down Fido’s throat.

Pet drugs enjoy the same patent protection as human drugs but they are also buttressed by softer moats, like brand familiarity and trust with veterinarians. They're less capital intensive, too, requiring tens of millions rather than hundreds of millions of dollars to develop. And they're sold directly to somewhat price insensitive consumers, side-stepping a third-party payer system that, in human pharma, steers demand toward lower-cost alternatives and gives rise to globally scaled generic competitors. As a result, pet drugs – compared to livestock and human drugs – tend to be far less exposed to the cliff risk that usually accompanies generic launches.