[AME] AMETEK

AMETEK was birthed out of failure. After its predecessor, Manhattan Electric Supply Company, a supplier of electrical switches, telegraph sets, alarm clocks, flashlights and other novel gizmos of the late 19th/early 20th century, declared bankruptcy in 1930, months after the market crash, shareholders created a new company from the ashes. The newly formed American Machine and Metals sold heavy machinery (Troy Laundry Machinery) used by commercial laundry facilities to wash and starch clothing, and industrial centrifuges (Tolhurst Machine Works) used by wastewater treatment operations and pharmaceutical companies to isolate liquid components.

In the decades following the wartime boom, AMM diversified away from industrial machinery and toward the instruments and motors that would come to shape its modern identity, acquiring a presence in pressure and temperature gauges (US Gauge; 1944), small electric motors for vacuum cleaners (Lamb Electric; 1958), lab instruments (Mansfield and Green; 1965), and water filtration products (Plymouth Products; 1967), among other product niches. Along the way, they changed their corporate name to AMETEK. Under the leadership of Dr. John H. Lux, who presided over the company as CEO and Chairman from 1969 to 1990, AMETEK did a bunch more acquisitions in this general vein across a variety of industries, including monitoring devices for commercial aerospace. They also divested a dozen non-core businesses in 19881 and expanded overseas to take advantage of a globalizing economy.

By the time Dr. Lux retired as Chairman in 1993, about 38% of AMETEK’s revenue came from Electromechanical Group (EMG), which primarily made electric motors for floor-care products (vacuum cleaners) but had expanded into doing the same for lawn tools, photocopiers, and computer equipment. Another 38% of revenue came from Precision Instruments, which manufactured cockpit instruments, jet engine sensors, and electronic systems that recorded flight and engine data. AMETEK sold similar instruments, designed to measure force, speed, pressure, and temperature, into heavy trucks, ag equipment, petrochemical plants, and various other industrial applications. The rest of AMETEK’s revenue came from Industrial Materials, a grab bag of products that included water filters (residential and commercial), storage tanks, and specialty metals and plastics.

AMETEK’s Precision Instruments segment, geared as it was to aircraft instrumentation, was hit hard by a retrenchment in commercial and military aerospace demand in the early ‘90s. While revenue had grown 25% over the previous 4 years, profits had gone nowhere and margins contracted, even excluding one-time restructuring charges. The stagnating financials prompted asset write-downs and a major restructuring effort geared toward controlling costs and expanding floor care motor capacity.

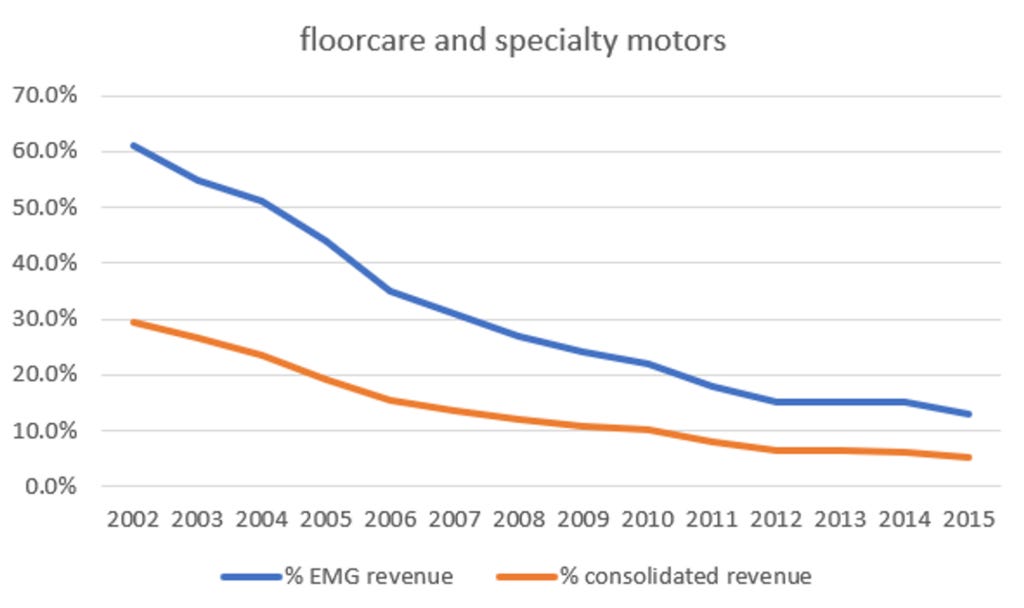

By 2004 AMETEK was in a better place, with $1.2bn of revenue spread across a more diversified set of markets and EBITDA margins cresting 20%. Still, one of their largest business lines had gotten commoditized by then. In 1993, electric motors for vacuum cleaners and home appliances was seen as a major growth opportunity. By 2004, these product lines, which accounted for just over 50% of EMG and 23% of consolidated revenue, were beset by price-led competition from Europe and Asia. Over the following decade, as AMETEK continued to acquire businesses with lower capital requirements that compete on product features rather than price, the contribution from floorcare and specialty motors was whittled down to so small a size that after 2015 its revenue was no longer separately disclosed.

Meanwhile, management began calling out the proportion of EMG revenue coming from “differentiated” businesses, which it classified into 2 buckets: