[BUR/LN – Burford Capital] Part 1: Industry context and competitive advantages

Law firms are staid institutions, averse to change and culturally ill-suited to bearing risk on high stakes IP and contract disputes, bankruptcy cases, and competition claims1. Their partners don’t hold permanent equity interests and so rather than invest in the long-term health of the business, they extract as much profit for themselves as possible before they retire. But while law firms have long resisted change, their corporate clients have been demanding more of it. Under mounting pressure to bracket costs, clients have been pushing law firms to relent on the long despised hourly billing model and consider contingent fee arrangements. A few years ago, Microsoft famously eschewed bill-by-the-hour in favor of success-based pricing.

The problem is that even law firms that want to accommodate contingent payment models are resource constrained and find themselves with limited access to outside capital: banks, accustomed to lending on hard collateral, don’t know how to underwrite legal risk2 and certain ethical rules in the US prevent non-lawyers from taking ownership stakes in law firms, foreclosing equity raises. That’s where litigation finance comes in. An enterprising law firm offering its clients success-based pricing might turn to a commercial litigation financier like Burford, who commits to funding a fixed amount of the client’s legal expenses on a non-recourse basis (the client is under no obligation repay the capital). In return for exposing its entire investment to loss if the matter doesn’t resolve in the client’s favor, Burford stands to make many times its money in the event of a favorable settlement or adjudication3. Clients, meanwhile, transform uncertain and unpredictable legal expenses – the kind that eat into the above-the-line profits that shareholders scrutinize – into an option on a successful legal outcome.

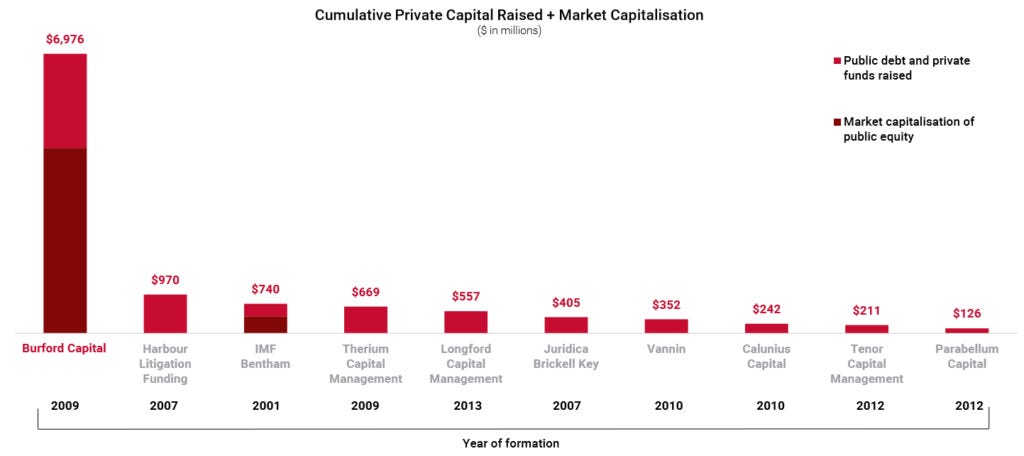

Burford competes with a handful of notable litigation funders, most of them private. In terms of funds raised, which I suppose Burford sees as a reasonable proxy for other relevant measures of scale like capital committed and deployed, Burford is by far the largest:

Burford’s $1.4bn of book value and $1bn+ of claimed recoveries to date exceed the $368mn and $600mn, respectively, reported by Bentham, one of the few other notable publicly traded competitors. Over the last 2 fiscal years, Burford has deployed 7x as much capital as Bentham. Management cites supposedly independent surveys in which 63% of lawyers name Burford when asked “what providers of litigation finance are you most familiar with?”, with only 10% citing a competing firm.

While lofty returns have attracted competition, those who have tried to break in have failed to scale to anywhere near Burford’s level, suggesting that there may be a moat.

Because funding is commonly dripped out in tranches and tied to milestones, law firms with complex, long-duration cases will go with a stable capital provider, one with enough portfolio diversification – across geography, law firms, economic structures, claim types (IP, contract, bankruptcy, etc.) – to withstand the binary outcomes typical of litigation financing. While Burford has generated outsized payoffs from its winners, investments comprising 15% of capital deployed since inception have lost 90% or more of their value. Even if the expected value of litigation financing is positive, a small shop with a few single case deals may go bust before the law of large numbers bears this out.

Burford’s diversified portfolio immunizes the company from catastrophic risk. Its largest law firm relationship accounts for 17% of investments across 50 partners while its largest outstanding balance sheet commitment is for $127mn, just 10% of tangible equity. And that chunky commitment backs a cross-collateralized portfolio of cases that is insulated from the yolo payoff characteristics of single deals (all of Burford’s 90%+ losses have been in single-deals; none of its portfolio finance investments have lost money). [Portfolio finance investments aggregate multiple (often unrelated) litigation or arbitration cases under a single funding vehicle]

One might argue that some sovereign wealth fund could just shoot billions of dollars into the space and build a diversified portfolio from the get-go. This wouldn’t work in practice for several reasons.

First, litigation financing is not just about the money. While litigation funders don’t directly manage cases day-to-day, they can lend a second set of expert eyes. To optimize the value of its investment, Burford might help prepare arguments and craft strategy. A mature player like Burford that has seen thousands of cases might pursue legal avenues that a novice might overlook. For instance, Burford was once involved in one matter that spent two years in limbo before an appeals court ruled against Burford’s client. But rather than just taking a 0, as an inexperienced shop might have, the company funded a second case against a third party who it determined was ultimately responsible for the loss. That case ultimately resolved in favor of Burford’s client and Burford made 3x its investment over 3 years. Or consider the Petersen case, a complicated matter in which the liquidators of a Spanish energy company, Petersen Group, sued YPF (the oil major in which Petersen held a 25% stake) and the government of Argentina (which nationalized YPF), in US courts. Burford is one of the few players in this space (maybe the only one) with both the legal expertise to underwrite a case involving entities from 3 different jurisdictions and the scale to comfortably handle the binary outcome of an $18mn capital deployment.