[BUR/LN – Burford Capital] Part 3: The short heard round the world

In this post, I offer thoughts on the Muddy Waters’ report. Some of its claims were valid, some were innocuous, and a few seemed so obviously flawed as to be postulated in bad faith. I was surprised by how readily the write-up was received as gospel truth. Twitter was inundated with self-loathing from former Burford bulls and cheap “told ‘ya so” talk from wise men who suddenly materialized out of nowhere. The few who were openly skeptical of the company pre-MW were roundly congratulated before Burford’s management team even had a chance to offer counterarguments, as if the case were officially closed.

Emotions run hot with the stock, so lest I be accused by both sides of harboring an agenda — I defend and criticize Burford at various points — I thought I’d make it clear up front that I don’t have skin in this particular game. I had no position in Burford at the time I published my original write-up and I don’t have one now (though, as always, this may change at any moment without notice!). My aim with this post, as with all my other posts, is to offer the most intellectually honest analysis that I can, not to “defend” a bull or bear thesis.

(All direct quotes from Muddy Waters will be bolded)

Let’s start with the Napo vs. Salix case.

“BUR’s reporting of Napo Pharmaceuticals Inc. v. Salix Pharmaceuticals Inc. (“Napo”, BUR case no. 111290) should make BUR investors want to take a shower…BUR first disclosed Napo as a “Concluded Investment” in its 2013 Annual Report, and claimed a total recovered of $15.8 million on a $7.4 million investment, which was purportedly a 113% ROIC. However, the case had not yet concluded. It reached a jury verdict in 2014, and BUR’s client, Napo, actually lost the trial when the jury returned a verdict in favor of Salix…The fact that Napo actually lost the trial in 2014 did not sour the company’s view of its investment. Rather than reverse the gain, BUR actually marked the investment up yet again – to a ROIC of 189%”

Muddy water’s makes two allegations here: first, that Burford jumped the gun and reported a gain on the Napo v. Salix case in 2013 when in fact that case did not even conclude until the following year; and second, that Burford failed to reverse that gain when in 2014, the ruling failed to turn in Burford’s favor.

But, according to management:

“…Burford structured its financing agreement with Napo so that its recovery could come from not just Napo’s dispute with Salix, but from other litigation as well. As it transpired, a litigation matter other than the Salix matter resolved first, and resulted in an entitlement for Burford. That is the figure shown in Burford’s 2013 reporting”

So, the Napo v. Salix dispute may not have gone Burford’s way, but Burford wisely structured the deal from the start so that its recovery could come from Napo’s other litigation cases as well. As it turned out, one of those other (non-Salix) cases resolved favorably in 2013, hence the $15.8mn recovery reported that year. I am on management’s side up to here.

But then things get weird.

While the Napo v. Salix case meanders through the litigation pipeline, Salix is acquired by Valeant and Napo IPOs its animal health business, Jaguar, in 2014, leaving Napo with the human health business. Burford restructures its litigation financing arrangement with Napo, converting its investment into Napo debt that later. Napo and Jaguar merge in 2017 and as part of the merger, Burford’s Napo debt is replaced with $8mn cash and shares of Jaguar (JAGX) valued at $20mn. So, from 2013 to 2017, Burford’s recovery in the Napo case transmutes from a non-Salix entitlement to Napo debt to cash + shares in Jaguar.

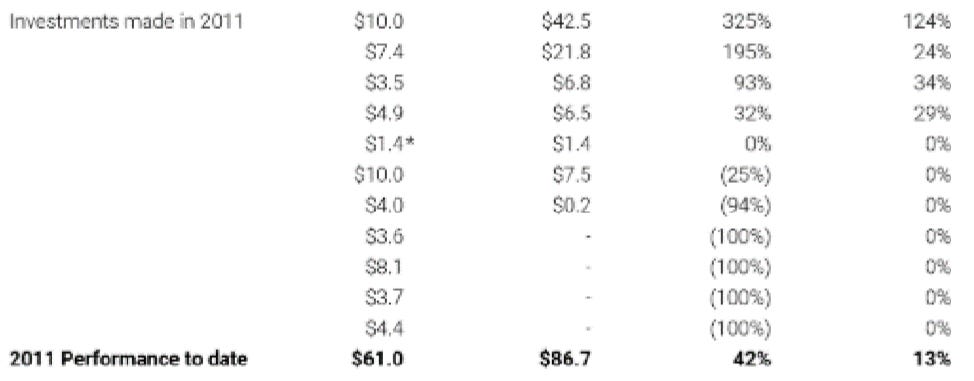

Here is how management reports the Napo investment on the ROIC table in 2013, after the non-Salix case paid off but before Burford got the $8mn cash + $20mn JAGX (via MW)…

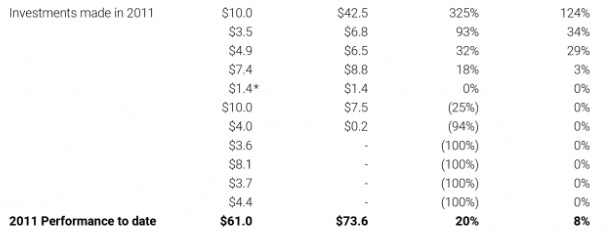

Here is how Napo is reported in 2017, when its recovery takes the form of cash + JAGX…

In its 2017 annual report, Burford writes:

“Because Jaguar is publicly traded in an active market, we are obliged to mark our equity position to market, which in 2017 caused an unrealized loss of $6.95 million as the stock price declined from a formulaic deal price at which our equity interests were initially issued (which we are reporting separately as “net loss on equity securities” on the income statement)”.

If we shave $7mn of unrealized losses off JAGX’s original $20mn value, that gets us $13mn. Add the $8mn of cash recoveries and we’re at $21mn, close to what we see in the 2017 table.

From year-end 2017 to 2018, JAGX gets smoked. Yet, in the 2018 returns table, the Napo recovery is still marked at the same $21.8mn that it was the year before.

JAGX is a publicly traded security, its value easily determinable. The stock’s mark-to-market was captured in book value (per IFRS) but for whatever reason, wasn’t baked into Burford’s returns table until recently, in the mid-year 2019 disclosure:

This is a red flag and MW is right to call it out.

Muddy Waters supplements this concern with the salacious allegation that Invesco, who was the largest shareholder of Burford in 2017 and so had a vested interest in saving Burford’s Napo investment, backstopped an equity offering from Jaguar, buying over 3mn shares of JAGX for $3mn, proceeds that Jaguar loaned to Napo and which Napo used to extinguish its debt to Burford1. MW alleges that Invesco’s participation in the equity offering “was made purely to perpetuate a mythical ROIC and IRR” at Burford, a claim bolstered by the fact that the same guy, Mark Barnett, manages a fund that holds a substantial stake in Burford (Invesco High Income Fund) and the fund that backstopped the Jaguar equity offering (UK Strategic Income Fund) [in its rebuttal call, management claimed that shares of Burford and Jaguar were held in Invesco funds managed by different managers, but it seems Burford is mistaken]

Invesco denied accusations of impropriety while Burford responded:

“One of Napo’s early equity investors was an Invesco fund run by Mark Barnett. Given that Burford’s institutional investors represent some of the largest investors in the world, it is not at all unusual for Burford to be providing financing to – or to be adverse to – companies held by its investors. The Napo investment was not introduced to Burford by Invesco, and at the time Burford had no relationship with Mr. Barnett, whose fund did not hold any Burford equity.

Out of those straightforward facts, the report attempts to outline a groundless conspiracy between Invesco and Burford (throwing in Neil Woodford’s name for headline value). Invesco was an equity holder in Napo, with all of the risks and returns associated with equity holders. Burford was a secured creditor. Invesco engaged in the actions it believed advantaged its equity investment in Napo, including participating in various rounds of equity investment in the business. Burford engaged in its own negotiations, which often disadvantaged Invesco given Burford’s senior position in the company’s capital structure. There was no complicity and not a moment’s thought that Invesco was making further investments in Napo ‘purely to perpetuate a mythical ROIC’ as the report suggests”.

(emphasis mine)