[CACC – Credit Acceptance Corp] Value in subprime auto

Most auto lenders won’t finance cash strapped buyers with deeply tainted or limited credit histories. Credit Acceptance Corp, founded in 1972 by Chairman and 11% owner Donald Foss1 to collect loans originated by his own dealerships, steps into the breach with an unorthodox lending scheme that goes like this: the used car dealer originates a loan2 to the deep subprime borrower and immediately assigns that loan to CACC. CACC pays the used car dealer ~45% of the contractually due payments up-front (“advance”). CACC then tries to collect from the borrower as much of the contractually owed amount possible (typically amounts to the company collecting 65%-75% of the contractual amount due), sharing 80% of collected payments with the dealer (the dealer “holdback”), with holdback payments diverted to CACC until the advance is fully recouped.

Below is an illustration of the IRR that CACC might realize on a typical loan3:

[While the contractual maturity of a loan is closer to 5 years, because CACC first recoups its advance from dealer holdbacks and borrowers are more likely to meet their loan obligations early on in a loan’s life, 85% of expected cash flows recognized within the first 3 years4.]

This model works for the dealer because: 1/ by lending to borrowers that others won’t finance, CACC expands the pool of car buyers for the dealer and 2/ with the advance from CACC plus the down payment from the borrower, the dealer recognizes an immediate gross profit of ~10%-20% of the wholesale cost. It’s a good deal for CACC because back-end profits incent the dealer to sell the borrower a car she can afford, improving the chances that the loan is repaid. Furthermore, dealers enrolled in this “Portfolio Program” (as management calls it) are rated according to the performance of their loans, and these ratings factor into the upfront advance that CACC is willing to pay. And so, CACC and used car dealers are essentially lending partners with aligned interests. CACC collects as much as it can from borrowers – typically 60%-70% of contractually due principal + interest, plus sales on repossessed vehicles, which constitute a minor ~mid-single digit % of collections – and keeps whatever’s left over after dealer holdbacks.

Now obviously, a dealer would prefer to assign the loan to someone like Nicholas Financial, Santander, Consumer Portfolio Services, and other subprime-y auto lenders who are okay underwriting to mid/high-single digit returns on capital and so pay 90c to 100c on the dollar upfront. But even those guys won’t underwrite the shakiest of credits most days. So dealers end up funneling the lowest rated borrowers to CACC, who says “yes” to every valid loan request and manages the risk from this ostensibly reckless practice by toggling the advance rate it pays to the dealer (the riskier the pool of borrowers, the lower the advance rate).

Starting in 2005, as it became clear that some large dealer networks had corporate processes that couldn’t accommodate novel contingent payment structures, CACC also began offering more traditional loans under its Purchase program, where it pays the originating dealer a higher one-time upfront payment for the loan and keeps all loan repayments (no dealer holdbacks). According to management, Purchase loans generate returns that are comparable to Dealer loans (“Program” loans) but are also riskier because the dealer’s incentive to underwrite diligently goes away; the loan is typically underwritten at longer maturities; and requires somewhat more capital upfront (48% of the contractual amount owed vs. 44%), raising the consequences of the loan being crappier than expected. Management would prefer to do Purchase loans. But in the 14 years that CACC has been underwriting them, Purchase loans have been very profitable and now account for 1/3 of the company’s total loan book.

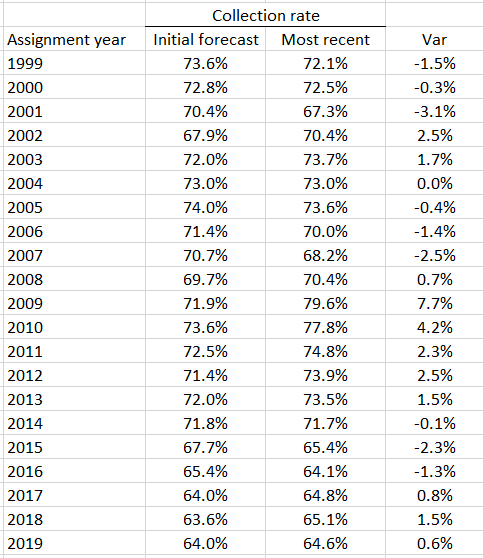

When the dealer assigns a loan pool, Credit Acceptance takes an initial guess of what percent of the contractually owed amount it will ultimately collect. As the loan pool ages, the company revises its original collectability estimate based on the how the pool is performing. Because there are no take backs on the advance rate, the initial forecast for collections is critically important. If CACC offers the dealer 45% of the contractual repayments as an advance because it expects to collect 65% of the contractual amount from borrowers but actually ends up collecting only 50%, the company can’t go back to the dealer and ask him to return part of the advance so that it can hit its return bogey. Assuming CACC is doing its job well, updated estimates should hew closely to the original forecast of loan collections, which is exactly what we see:

The “most recent” column is management’s estimate of the collection rate for each vintage year 10 years after the original forecast, assuming, of course, that 10 years has passed…if not, we’re looking at the estimate as of the most recent quarter (4q19). Since the initial term on a CACC loan is around 4-5 years, after 10 years, the company’s “most recent” estimate for older assignment years should very accurately reflect the true performance of that vintage year.

To home in a specific case, the company originally thought it could collect 69.7% of the amounts it was contractually due from the 2008 vintage of borrowers; the most recent estimate of that vintage’s collection rate is 70.4%. The “Var” column shows the most recent estimate minus the initial forecast, so a negative number means that CACC collected less than expected, while a positive number means that CACC collected more than expected. In its worst forecasting year (2009) the company was off by ~11% from its original estimate…and that was because it underestimated ultimate collections, a “good” mistake. The most management has ever overestimated collections for any vintage year was 4% (2001). Moreover, it appears that management has been more conservative in its initial forecast for Purchase loans vs. the Dealer loans5, perhaps to account for the latter’s higher risk and the company’s relative lack of experience underwriting it.

You’d prefer that the initial forecast be lower rather than higher than most recent estimate, but ideally there should be no difference between the two at all because the key metric that CACC is trying to maximize is economic profits, which is a function of both unit profits and volumes: