[CSU] Constellation Software

The fawning adoration that investors heap on certain capital allocators can be a little gross, but Mark Leonard, CEO of Constellation Software1, deserves most of it. His letters are a master class in lucid and honest communications and a welcome reprieve from the enervating, mealy-mouthed crap that we hear from lesser CEOs all year long. Mark doesn’t seem self-conscious about couching his statements in caveats or acknowledging trade-offs. Nor is he too proud to learn from other successful conglomerate businesses (going so far as reaching out to current and former Illinois Tool Works employees several years ago to learn from their decentralized business model). And his shareholder-first sentiments are backed up by action. For instance, in deciding to devote fewer hours to work to live a more balanced life, he wrote the following in Constellation’s 2014 Annual Letter:

“I’ve been the President of CSI for its first 20 years. I have waived all compensation because I don’t want to work as hard in the future as I did during the last 20 years. Cutting my compensation will allow me to lead a more balanced life, with a less oppressive sense of personal obligation. I’m paying my own expenses for a different reason. I’ve traditionally traveled on economy tickets and stayed at modest hotels because I wasn’t happy freeloading on the CSI shareholders and I wanted to set a good example for the thousands of CSI employees who travel every month. I’m getting older and wealthier and find that I’m willing to trade more of my own cash for comfort, convenience, and speed … so I’m afraid you’ll mostly see me in the front of the plane from here on out”.

If this were about almost any other investor/CEO, I might counterpose that “straight talk” is its own kind of artifice, a ploy to pander to investors who like that kind of stuff2. In Mark’s case, if it is pandering, then it’s good business too, as there are legitimate reasons for Constellation – an investment vehicle with a value-oriented, multi-year time horizon – to attract the right kind of shareholders and employees.

My Tyler post from last week may have elicited comparisons to Constellation Software. But the two companies differ in many ways. Aside from surface level considerations – Constellation sells to private companies as well as public entities, generates far lower organic growth, acquires far more companies, and funnels more of its free cash flow into acquisitions – Tyler firmly identifies as a software company that strategically uses acquisitions as a means to build a bigger and better software business3, while Constellation is a capital allocation vehicle that just happens to invest in software.

Despite building a $3bn revenue company on VMS, you get the sense that Mark is agnostic about the business of VMS itself and would have no qualms directing capital to non-software or returning capital to shareholders were its current opportunity set in software to ever run dry, though with somewhere between 35k and 50k software companies on its target list (vs. 500+ acquisitions made since inception), with new software businesses being spun up all the time, this is still some time away. When Tyler references the competitive differentiation that results from its numerous acquisitions, it is referring to wide product breadth and integration potential. By contrast, Constellation’s ~500 business units are more like a test bed that provides proprietary “base rates” against which to evaluate the assumptions being used to justify potential deals, run (and kill) small-scale experiments, and benchmark the results of one business against another, so that best practices can be shared across units (for instance, based on a past experience, Constellation can gauge how much they can raise prices before churn becomes a problem). Even the titles that Constellation assigns to organizational roles emphasizes the centrality of capital allocation: a business unit manager who executes several good acquisitions might be promoted to “Portfolio Manager”, whose job it is to find new investments and monitor various business units; a Portfolio Manager with a distinguished track record earns the “Compounder” designation.

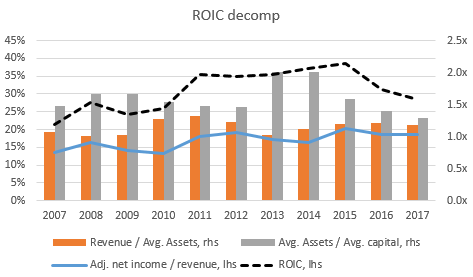

You will hardly ever hear Mark talk in depth about the operations of Constellation’s software businesses, who all operate independently for the most part. The company’s aggregated sales and profit figures are not the product of a grand, top-down vision executed across business units sharing a cohesive mission, but rather the emergent property of many small businesses – each ranked #1 or #2 in a market of rational competitors, that sell mission critical software with high retention rates (90%+) – offering varying levels of customization, operating across a wide range competitive environments. The Constellation story is predominantly about disciplined capital allocation rather than exceptional growth at the Business Unit level. Instead of honing in on any one business unit, time is better spent understanding the organizational structure and economic incentives that enable returns like these:

[Note: Invested capital, in this case, is basically computed as net income + amortization expense divided into retained earnings + accumulated amortization. Constellation typically holds very little debt on its balance sheet, so ROIC =~ ROE.]

The discernment that management has applied in its acquisition process is reflected in the company’s stellar long-term track record: out of the 500+ companies that Constellation has purchased over the decades, the number that have failed to meet their return hurdles or suffered impairments can be counted on fewer than two hands.