FICO and the Consumer Credit Bureaus: Part 2

From the early 2000s to now, EET have evolved from credit reporting agencies selling indistinguishable datasets to information technology companies offering predictions1. Over time, all 3 bureaus have gotten bigger, their delivery mechanisms have changed (from phone calls and paper reports to software), their data sources have expanded – to encompass different kinds of data (alternative data2), across time (trended data3) – and their analytics have gotten more advanced. But they’ve all basically abided by the same playbook since the ‘70s: acquire datasets, bundle the datasets with analytics, and export products and technology to other industries and countries.

The US agencies have established footprints in foreign countries by either: 1/ partnering with banks and credit card associations to develop a country’s first consumer credit agency (as TransUnion did in India and the Philippines) or 2/ acquiring or taking minority stakes in incumbent foreign credit agencies who enjoy the same oligopolistic positions in their respective countries they do in the US (as Experian did in Brazil and Colombia). Expanding overseas makes sense because the use cases for bureau data and analytics don’t really vary much across countries.

The rationale behind industry diversification is more complicated and case specific. At some point in their lives, each of the bureaus (and FICO) has tried building mass outside of financial services, mainly in insurance, healthcare, and retail. Those industries are similar to financial services in that they touch just about every middle-class consumer; migrate through a well-defined customer lifecycle, from acquisition to management to collections; and wrestle with product optimization, marketing, and fraud, areas where analytics bear relevance.

Here is the mix of b2b revenue that the credit bureaus derive from various sectors (note: TransUnion is US only):

[Financial services includes credit cards, mortgages, and other types of loans]

That the bureaus are so dominant in financial services is largely the result of historical circumstance (with credit taking off post-WW2, regional credit agencies were begging to be rolled up) and path dependency (feedback effects between data breadth and client adoption), so it’s perhaps no surprise that these advantages haven’t easily carried over to other domains.

Equifax divested substantially all of its healthcare and insurance initiatives in the late ‘90s/early 2000s and these days when the company expands into other verticals, it’s more or less just repurposing credit data, not customizing apps that compete with entrenched competitors. The $1bn+ sized acquisitions that Equifax has made over the last dozen years (TDX, TALX, and Veda) are all grounded in widely applicable data or close extensions of the core credit reporting business.

In the early/mid-2000s, FICO had grand ambitions to extend its analytics to 20+ different industries, including aerospace and transportation, only to 5 years later soberly narrow its purview to banking, insurance, healthcare, and retail. But even this proved 3 verticals too many. Insurance and healthcare never scaled to meaningful size. FICO’s Retail Action Manager – which offered custom coupons to customers based on prior purchases – was heralded as the company’s next major franchise only to wither into oblivion 3 years later after its two marquee clients, Sam’s Club and Best Buy, terminated their contracts. Today, financial services clients make up 80% of FICO’s revenue vs. 70% in 2004, when the company embarked on its verticalization strategy.

Experian has diversified outside financial services post-GFC and like Transunion, has been particularly keen on healthcare (in 2014, management commented: “it would not surprise us if the healthcare business in the US eclipsed the core credit services business.”). As a percent of revenue, Transunion tilts more towards Healthcare than Experian though Experian is larger on an absolute basis (in fact, the latter has multiple $200mn+ revenue verticals outside of financial services). Since first getting into healthcare in ~2007/2008, both companies have acquired a slew of health-specific data/analytics assets to build out Revenue Cycle Management (RCM) products. [TransUnion has been selling credit reports to hospitals and physicians since the 1970s, but the bulk of its healthcare practice has been built since ’07, mostly through acquisition]

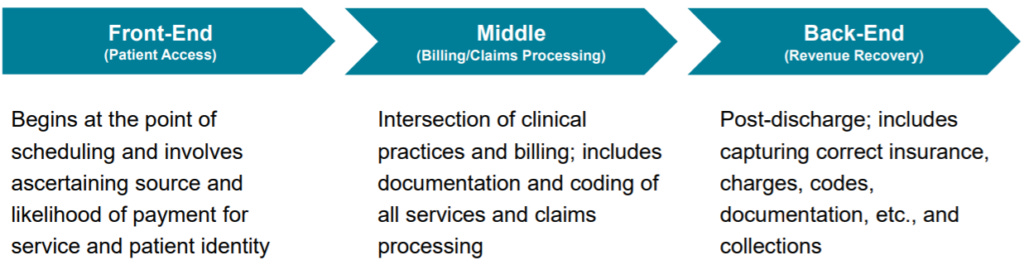

Revenue Cycle Management – helping healthcare providers maximize reimbursement – consists of 3 parts:

Without the domain expertise to play in the middle, TransUnion has been relegated to the front-end (patient access) and back-end (revenue recovery). Experian, on the other hand, with its $850mn acquisition of Passport Health in 20144, covers everything from appointment scheduling to billing to payment collection. It has dual purposed its existing fraud detection technology into patient information systems and more recently, has been positioning itself in as a Population Health Management solution (you can think of PHM as a consistent, longitudinal record for every patient across different disparate providers), launching Universal Identity Manager (UIM) as a patient key identifier across the fragmented databases of different hospitals, labs, pharmacies, and medical groups.

Besides healthcare, insurance is also a key growth initiative for TransUnion (Experian’s Insurance revenue is larger but comparatively smaller as a percent of revenue and not really a priority for the company). Like one of the things TransUnion does in Insurance is it runs analytics against a database of traffic violation court data so that auto insurers can more accurately price risk and don’t have to waste time and money pulling motor vehicle reports on drivers with clean court records.

TransUnion and Experian have done okay in Healthcare and Insurance, though perhaps not as well as one may have expected given the intense strategic attention both companies have paid to these domains. Since Passport, Experian has grown its Healthcare revenue by ~12%/year, faster than the mid-single digit organic growth it has realized elsewhere. TransUnion’s Insurance and Healthcare businesses are growing “double-digits” and “single-digits” (down from teens growth 5 years), respectively, with revenue from its Emerging Verticals – which includes healthcare and insurance, plus other industries outside financial services – growing ~high-single digits…which is not as good as the low-teens organic growth it is posting in its more mature core b2b (and the revenue is lower margin to boot), but still, not terrible.

Maybe the legacy processes in Insurance and Healthcare are so antiquated and desperate for resuscitation that just about any vendor with a plausible modern remedy can enjoy double-digit revenue growth up to a certain point. But what are the unique advantages TransUnion and Experian bring to these very crowded domains?