Is Global Payments the next Adyen?

(no, but that doesn’t mean it can’t be a good stock)

AI-generated podcast conversation: Spotify, Apple

AI-generated summary: Global Payments’ $24bn acquisition of Worldpay is the latest installment in the long-running saga of merchant acquirers trying to scale their way out of obsolescence. Less than a year after publicly swearing off M&A, Global is now pursuing a mega-deal that may make strategic sense in a vacuum, but directly contradicts its own stated strategy. The deal creates a formidable global acquirer, but also drags the company back into a legacy playbook of scale-first, integration-later. The setup? Messy, cheap, and not without upside – if investors can stomach the distraction.

I.

Last April, Global Payments announced that it would be acquiring Worldpay and divesting the Issuer Processing business obtained through its 2019 merger with TSYS, dismantling one monstrosity to create another. On the other side of the table, buying the business that Global is selling and selling the business that Global is buying, is Fidelity National, who had acquired Worldpay in a mega-merger of its own, only to sell a majority stake to private equity five years later after the strategic merits of the deal proved elusive. Scarcely in the history of payments have so many bankers been paid such enormous fees for so little value creation.

One could have hardly imagined what Global Payments would eventually become when it was spun-off National Data Corp.1 in 2001. Back then, merchant acquirers distributed payment processing services through two primary channels: banks, who owned the merchant relationships, and Independent Sales Organizations (ISOs), which you can think of as outsourced sales agents, though sometimes they evolve into something resembling the merchant acquirers they represent (Shift4, for instance, began as an ISO that sold payment processing on behalf of TSYS but eventually developed its own POS software and processed its own payments). As an independent company, Global Payments rolled up both, acquiring the merchant acquiring units of banks in Europe, Asia, and Latin America, and purchasing ISOs who catered to small and mid-sized merchants here and abroad.

Then, software ate the world. Merchants who traditionally sourced card processing services through banks and ISOs increasingly did so through the software they used to manage their operations. No company embodied this seismic shift in channel strategy more than Stripe, who hid the complexity of payments acceptance behind a few lines of code that developers embedded in SaaS applications. Within this milieu, Global Payments was a fusty incumbent, out of step with the times. Tethered to legacy distribution models, it endured seven years of slowing growth, margin erosion, and anemic shareholder returns, culminating in the retirement of its long-time CEO Paul Garcia. But just before Paul stepped down in 2013, Global acquired Accelerated Payment Technologies, taking the first meaningful step toward what came to be known as “integrated payments”, where core payments processing is integrated with third party software (in APT’s case, software used by dentists, vets, pharmacies, and merchants across many other verticals).

Jeff Sloan, Paul’s successor, sprinted with the baton, shelling out ~$1bn on growthy, margin-accretive integrated payments providers and e-commerce gateways in the span of just a few years. To put distance between itself and the ever more commodified business of payments processing, management began saying stuff like: “We are not a processor, we are not a payments company, we are not an acquirer. We are a technology provider to these customers who need to have these types of integrated interactions with their consumers”.

But, if you have to declare something like that out loud, it probably isn’t true to the extent you’d like it to be. Integrated payments was an improvement over the bank and ISO-led distribution of yesteryear in that it piggy-backed on growing software adoption. Still, under this model, payments is not entirely one with the software. The merchant acquirer and the independent software vendor (ISV) are two distinct entities. Each strikes their separate agreement with the merchant, who can work with any of the acquirers the ISV integrates with.

By contrast, in Embedded Payments the ISV doubles as the payment provider. The central actors in this model are payment facilitators (or ”payfacs”) like Toast, Square, and Mindbody. Payfacs underwrite and onboard merchants under their own Merchant ID, which puts them on the hook for KYC and compliance violations, meaning if one of Square’s merchants vanishes without delivering products that were paid for or sells a product, like CBD oils, that runs afoul of card network rules, any resulting liability falls on Square. Whereas in an Integrated Payments setup a merchant signs two distinct agreements, one with with ISV for the software and another with the acquirer for payments processing, in Embedded Payments a merchant signs just one agreement, with the ISV, who in turn either processes payments themselves or, more commonly, strikes an agreement with a third party processor. So, a restaurant using Toast as its POS typically doesn’t know – nor does it need to know – that Worldpay is ultimately processing payments beneath the surface. Toast has an agreement with Worldpay; the restaurant does not.

Global Payments offers two related but distinct payfac-oriented services. In the first, as a white-label processor for the payfac, it routes payment authorization requests through the card networks and settles funds to the payfac’s account, steering clear of merchant underwriting risk. In the second, as a program facilitator (or “profac”), it assumes the full responsibilities of a payfac on behalf of software vendors and online marketplaces.

But why stop there? Why not climb still further up the value stack, owning not just the payments or merchant onboarding layer, but the software itself? In that spirit, in April 2016 Global Payments made its largest purchase to date, acquiring for $4.4bn (~13x post-synergy EBITDA) Heartland Payments, the 9th largest US processor by volume at the time, whose coverage included a significant presence in restaurants, retail, convenience stores, K-12 schools and colleges. In owning the POS software, onboarding, and core processing, along with a direct salesforce to reach merchants (Heartland’s founder was philosophically opposed to ISOs), Heartland was about as vertically integrated as it gets. Global then spent another $2.3bn to acquire three vertical SaaS vendors2, aiming to replace their merchants’ existing acquirer relationships, using discounted software rates as a lure – a strategy not dissimilar to Shift4’s approach of loss-leading with POS software and monetizing through payments (the astute reader will recognize that these SaaS vendors are not payfacs in that they require each underlying merchant to have their own merchant account).

From an enterprise value of just ~$3bn in 2012, Global spent $8bn on growthy forward-looking acquisitions, until by 2018 nearly half its revenue came from integrated payments, e-/omnichannel commerce, and vertical software, business lines that hadn’t existed prior to this transformative journey. In the heady days of the late-2010s, with the market gushing over software, management encouraged analysts to value the company on a sum-of-the-parts basis.

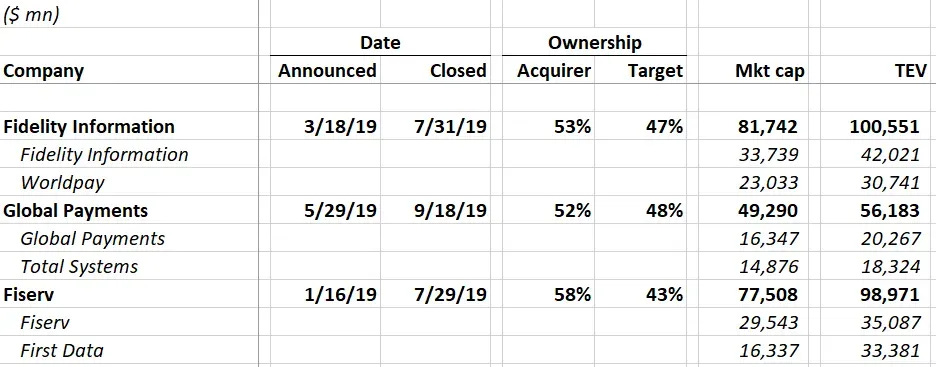

It was around this time when Global Payments and Total Systems (TSYS) smashed together in a humungous $56bn merger of equals, closely following the combinations of other legacy merchant acquiring/issuer processing peers:

To understand the logic motivating this merger, we first need to build up to what TSYS was about at the time.

TSYS traces its origins all the way back to the early ‘70s, when it was conceived as a mainframe-based transaction processing engine for Columbus Bank & Trust’s card program, a service that was then extended to other card issuing banks. In the decades after its partial spin off from CB&T in 1983, TSYS won ever larger, more complex portfolios and expanded internationally, eventually growing into one of the leading independent issuer processors. TSYS then expanded into merchant acquiring during the ‘90s, its first notable presence marked through a 50/50 joint venture with Visa, which it came to fully own a decade later. With its US issuer processing business slumping by 40% during the GFC on the collapse of two large clients, Wachovia and Washing Mutual, TSYS doubled down on the merchant side through a flurry of M&A3, so much so that by the time it merged with Global Payments in 2019, its Merchant Services segment nearly rivaled Issuer Processing by revenue.

Unlike TSYS and Global Payments, Worldpay didn’t evolve from a single corporate lineage but instead was born through combination of two: Vantiv and, um, Worldpay.

Vantiv was founded in 1970 as a subsidiary of Fifth Third Bank, focused on processing electronic funds transfers. In the early ‘90s, it pushed into merchant acquiring, establishing a strong presence among the top 100 US retailers. Desperate for capital in the fallout of the GFC, in 2009 Fifth Third sold 51% of Vantiv to Advent International, who then took it public three years later. Freed from Fifth Third’s constraints, the newly independent company struck merchant referral deals with banks it had once been barred from courting and, echoing Global Payments’ playbook, pivoted away from traditional bank and ISO channels. After it IPO’ed in 2012, Vantiv began buying its way into integrated payments and e-commerce, most notably with the $1.9bn acquisition of Mercury Payment Systems, which deepened Vantiv’s reach into the SMB market through POS software integrations.

Worldpay, established in 1989 as a subsidiary of NatWest, a UK bank, initially focused on merchant acquiring and payment gateways, before expanding into e-commerce transaction processing by the late ’90s. In 2000, Royal Bank of Scotland (RBS) acquired NatWest, folding the latter’s merchant acquiring arm into its own and using the combined platform as a springboard for expansion. Over the next decade, RBS stitched together acquisitions and merchant acquiring partnerships across continental Europe, transforming Worldpay into one of the world’s largest payment processors. When the financial crisis crippled RBS’ balance sheet, the beleaguered bank was forced to divest non-core assets as a condition to receiving government aid. One of those assets was Worldpay, 80% of which was sold for £2bn to Advent International and Bain Capital, who took it public in 2015. In 2017, Worldpay merged with Vantiv in a $12bn transaction, with the combined entity retaining the Worldpay name.

So, Vantiv scaled integrated payments and card-present retail within the United States, tilting toward SMBs, while Worldpay delivered e‑commerce and cross‑border expertise, indexing toward global enterprises. Together they offered merchants an “omnichannel” platform spanning in‑store, online, and mobile payments acceptance almost anywhere in the Western world. A few years later, Worldpay itself was swept into an even larger deal, merging with FIS – a leading issuer processor with its own long, intricate history that I will not get into – to create a payments behemoth worth over $100bn.

II.

Phew. I mean, just an absolutely bewildering frenzy of acquisitions that go so many layers deep and encompass so many different processing engines across so many geographies that it comes as no surprise whatsoever that all attempts to consolidate them have utterly failed and long been abandoned. First Data tried for close to a decade before giving up. Vantiv eventually dropped the phrase “single platform” from its 10K. Adyen scanned at the mosh pit and rightly determined that the only way forward was to “start over again”.

But these issues were understood well before the crescendo of mammoth mergers in 2019. So, why’d they all go through with it? What was the point? There were the cost synergies, sure, which summed to 13% of combined EBITDA across all three mergers. But what strategic purpose did these transactions purport to serve?

Well, for one, it was thought that combining an issuer processor with a merchant acquirer could enable more accurate fraud screening that reduced the rate of false positives. In a typical card transaction, the payment authorization request hops from the terminal to the acquirer processor (Global Payments, First Data), across the card network (Visa, Mastercard) to the issuer processor (FIS, TSYS) of the card issuing bank, which approves or denies the transaction. So, by serving both the cardholder’s bank and the merchant’s acquiring bank, Global Payments could capture data on both sides of a payment transaction, yielding more and better data that results in sharper fraud modeling and higher authorization rates. For example, a standalone acquirer might flag as suspicious a purchase attempt from a foreign customer and decline the transaction. But if the acquirer is integrated with the issuer processor, it might see that, actually, this cardholder has a history of similar transactions that were approved without incident.

To be clear, this is different and not nearly as seamless as a true “on-us” transaction, where the issuing and acquiring bank (not just their processors) are one and the same. JPMorgan, for example, issues roughly 20% of U.S. credit cards, controls a similar share of U.S. merchant acquiring volume, and runs the processing engines for both. So, when its cardholders transact with its merchant clients, JP Morgan is essentially talking to itself. Merely owning the processing engines – but not the banks – on both ends doesn’t bypass network routing or deliver the same benefits. Still, in theory, sharing data and coordinating fraud signals across both sides of a transaction could give Global and TSYS a small but measurable edge in authorization rates, which matters when mediating payment volumes at massive scale.

The mergers were also motivated by cross‑selling opportunities and shared distribution. Fidelity, for instance, could push Worldpay’s merchant services through some of the 45 of the world’s 50 largest financial institutions it counted as clients in fast‑growing markets like Brazil and India, while tapping into its network of regional bank customers in the US. Likewise, TSYS could sell issuing to Global’s bank partners and Global could sell merchant services to TSYS’ and the combined entity, it was believe, would then have a better chance at securing joint ventures with large banks abroad, who were more inclined to purchase from a vendor that could offer both. Moreover, Global and TSYS were nowhere close to First Data or Worldpay’s merchant acquiring scale in the US, so merging their respective divisions together had a certain logic to it, especially as both were pursuing the same SMB and software-integrated strategy.

Today, the FIS/WorldPay and Global/TSYS combinations are widely recognized as having been a huge waste of time and a failure in certain respects. Anticipated improvements in auth rates from combining issuer and acquiring processing have never, as far as I know, panned out in practice. This seemed entirely predictable given that these issuing processing and acquiring systems ran on different technology stacks, each strangled by its own skein of legacy code. Even before their respective mergers, First Data and TSYS each ran issuer processing and merchant acquiring under the same roof and it’s not like either earned a reputation for best-in-class authorization rates or fraud detection. Whatever the theoretical advantages from occupying the issuer and acquiring ends were, I suspect, thwarted by the interoperability gaps inherent in managing vast archipelagos of disparate processing platforms. So, why would a scaled up version of the same setup, still hampered by fragmentation, yield a different outcome? (It didn’t).

FIS actually exceeded the revenue synergies it set out to realize through its merger with Worldpay. But that victory paled in comparison to the value destroyed through botched strategy and execution within the SMB cohort that made up ~25% of its merchant acquiring portfolio. The only time investors in legacy acquirers ever seem to hear the ugly God’s honest truth about how things are going is when it comes out of the mouth of a new CEO, when the incentive to come clean and heap blame on the prior regime are at their peak. Prior to Gary Norcross’ ouster in late 2022, if all you had to go on was management’s commentary, you’d think pretty much everything was right on track. Only after his departure did management fess up to a reality that was obvious to everyone: that Worldpay was hampered by “product gaps”, leaned too heavily on traditional bank and ISO-led distribution, and arrived late to software-embedded payments. The result? A stunning $17.6bn goodwill impairment of FIS’ Merchant Services division.

Legacy acquirers are masters at financial engineering but amateurs at organic development and execution. Their hungry eyes are sensitized to the nickels of cost synergies laying right before them and blind to the dollars that could be captured further down the road by tuning in to marketplace realities and adapting accordingly. It’s rather telling that when FIS’ management finally announced, in February 2023, that it would be spinning off Worldpay, the reason it gave for doing so was not that the company could, as an independent entity with aligned incentives, develop better products and re-think distribution strategy, but instead that FIS had “gotten into a tough spot with our balance sheet, whereby we don’t have the M&A capital to continue to commit and help grow that business”. From their perspective, the path to value creation is carved not through self-help initiatives but by “buying product and distribution, putting on the platform and then distributing growing revenue and EBITDA”.

The Worldpay spin-off idea was later scrapped in favor selling a 55% stake to GTCR at an implied valuation of $18.5bn (9.8x EBITDA, 10.4x including contingent consideration), with FIS retaining the other 45%. Under this new ownership structure, Worldpay intended to pursue the same ol’ acquisition-driven strategy, funded by $1.25bn of equity capital from GTCR and led by Charles Drucker, who previously served as CEO of Vantiv, which he scaled through M&A before selling to Worldpay4.

Then, this past April, GTCR and FIS agreed to sell Worldpay to Global Payments as part of a three-way asset swap, wherein Global would purchase all of Worldpay for ~$24bn (~8.5x synergized adj. EBITDA for the buyer, Global; 10.5x for the seller, FIS) and sell Issuer Solutions – the issuer processing business it acquired through TSYS – to FIS for $13.5bn (~12.3x adj. EBITDA for Global; 9x for FIS, including synergies). The net effect is that Global will pay ~$10.8bn for ~$1.6bn of 2025E EBITDA (~6.7x ), inclusive of $600mn of run-rate cost synergies.

The deal further cements Worldpay’s position as the largest global merchant acquirer by volume and unglues the awkward pairing of a merchant acquirer and issuer processor, in its placing creating a somewhat more coherent combination between two merchant acquirers.

Source: Global Payments / Worldpay merger presentation (4/17/25). Including stock-based compensation, Global’s standalone EBITDA margin is ~3 points lower.

III.

So then why did Global’s stock plunge 17% upon the deal’s announcement? Why does it continue to trundle along multi-year lows?

To understand the basis for this negative reaction, one needs to recognize how abrupt a U-turn this titanic acquisition was from what was being promised to shareholders at the time.

While Global’s acquisition of TSYS was not as mishandled as FIS’ of Worldpay – Global’s Issuer Processor revenue grew by ~5%/year while margins expanded – nor was the strategic logic of combining both sides of the ecosystem ever validated, as even Cameron Bready admitted after taking over as Global’s CEO in 2023 (again, mistakes are acknowledged only after regime changes). It seemed obvious to even a casual observer that Global primarily wanted TSYS for its merchant services business and that issuer processing was not a priority. Aside from the questionable strategic logic of owning it, TSYS’ issuer processing business involves long sales cycles and decade-long enterprise-scale contractual engagements with huge banks, a model foreign to a merchant acquirer accustomed to selling through software to SMBs at a far more rapid cadence. Even if Global wanted to make something of issuer processing, it’s not clear what or how. TSYS was strong in credit cards but weak in debit and core processing, placing them at a distinct disadvantage to Fiserv. Merging TSYS issuer processing with FIS, who is over-indexed to debit, clearly makes far more sense.

But even with this incongruent issuer processing asset dangling off to the side, Global seemed to at last be finding its bearings, steered by a new CEO who was forthright in his assessment that future success would require severing past practices.

Look, the path we had been on for the last decade is not the one that was going to continue to drive long-term growth and success for our business. We needed to make some changes in how we operate, how we’re organized, how we invest, to deliver better return on invested capital in our business to be more focused as an enterprise and really lean into the areas of differentiation we have in the marketplace today and stop doing some of the things that, frankly, weren’t driving the kind of returns that we needed to create for the business.

The new Global Payments would be operationally simpler and strategically focused, its agenda whittled down to just a handful of core initiatives.

First, it announced plans to shed non-core business lines and somewhere between $500mn and $600mn of associated revenue, a target that has now been met – with the sale of AdvancedMD (~20% of Global’s software portfolio) and the pending divestiture of the payroll business – and is likely to be upsized with management further “re-evaluating portfolio composition” following the Worldpay merger. Management remains committed to the vertical software strategy as a whole. It’s just that AdvancedMD was uniquely burdened by bespoke requirements specific to the healthcare industry that would have required lots of additional investment to meet, consuming resources from other initiatives that could be scaled across Merchant Services. Moreover, the outright ownership of a healthcare-oriented ISV created channel conflicts with a growing number of healthcare-focused software partners who came to Global through the TSYS acquisition.

Second, mirroring Shift4’s unification of POS brands under the SkyTab label, Global Payments began to consolidate, under the “Genius” brand, sixteen or so scattered POS software lines that had accumulated through years of frenzied M&A and were never properly integrated. This isn’t a wholesale, soup‑to‑nuts rebuild of a brand‑new platform, but nor is it merely a cosmetic reskin. Global built a cloud‑based solution packed with all the fixings – online ordering and delivery, accounting, marketing, loyalty – and are now in the process of migrating existing clients over. Launched for restaurant and retail verticals last quarter, with an international rollout planned for the second half of this year, Genius may be Global’s single most significant product initiative, an opportunity to resolve the confusion wrought by legacy fragmentation, a test of its ability to organically build and market a modern solution that can compete on an even plane with the slew of modern, vertically integrated systems – like Clover, Square, Toast – that it has lost share to for so many years.

Third, echoing its standardization push in POS, Global announced plans to consolidate its fragmented collection of standalone units into a more cohesive Merchant Services business – one that shares centralized functions and unified development standards. The messaging around this initiative was vague, but at least underpinned by a concrete $400mn cost savings target (~10% of pre-Worldpay EBITDA) by 20275. Acknowledging that it couldn’t be “all things to all customers in all markets,” Global aimed to reshape itself into a leaner, more focused battleship, concentrating its firepower on SMBs, engaging selectively with enterprise clients, and focusing only on verticals where it already had meaningful traction.

Finally, at its 2024 Investor Day, management issued a welcome repudiation of transformative M&A, opting instead to return $7.5bn, ~25% of its market cap at the time, to shareholders through dividends and buybacks over the next three years (~90% of the $8.5bn-$9bn of free cash flow that it expected to generate), and pivoted to doubling down on existing advantages and extracting more value from what it already had (“the wingspan of sustainability is organic growth”), almost apologetically conceding that it may do “limited tuck-in” transactions but that if it does, ROIC bogeys and investment grade leverage thresholds and strategic integrity will all be respected, pinky swear.

So, you can imagine how jarring it must have been when less than a year after that elaborate song and dance, management announced that $10.8bn in cash and shares would be going out the door for yet another mammoth-sized transaction! To be fair, this recombination of assets is far more sensible than the one it replaces. From the standpoint of scale and strategic sense at the industry level, it’s far better to have one huge issuer processor and one huge merchant acquirer than two separate entities, each combining smaller-sized versions of both. But that doesn’t then mean, as a Global Payments shareholder, you’d prefer to have Worldpay over not having it at all.

As far as merchant acquirers go, Worldpay and Global very different companies.

Worldpay, long associated with large grocers and big-box retailers, derives 70% of its volumes from enterprise merchants and counts global e-commerce, which accounted for ~30% of its transactions, as among its key strategic assets. In its global, upmarket orientation, the company most closely resembled Adyen, though in how each went about architecting their respective platforms, the two rivals could not be more different (when management boasts of the $3tn of volumes running across Worldpay’s platform, all I see is an opportunity for Adyen to triple in size!). Global Payments, meanwhile, catered primarily to SMBs, whom it accessed through thousands of domain-specific software partners. Both legacy players were built through an exhausting series of acquisitions – with most of those acquisitions the product of other acquisitions in turn – resulting in a patchwork of platforms so disjointed that merchants often find themselves juggling multiple contracts and reporting interfaces. Worldpay fulfills the promise of a comprehensive bundle of in-person/e-commerce payment services across the globe through a daisy chain of different systems that require separate integrations.

There is some value to smashing these two giants together. Payrix, a profac that Worldpay acquired in 2022, fits snugly within Global’s software-mediated approach and was growing north of 20%/year off a meaningful $300mn base prior to the merger announcement. Also, some of Worldpay’s enterprise grade omnichannel tooling, like FX optimization and alternative payment methods, can be carried down to the long tail of Global’s smaller merchants, who are increasingly demanding the same commerce capabilities adopted upmarket. And then, there are the usual synergies that have historically been used to justify deals like this – the distribution of Genius POS through Worldpay’s 6k-strong bank relationships; $600mn of expense synergies on a combined EBITDA base of ~$5.7bn.

However, this deal is also a titanic distraction and introduces yet another motherload of integration complexities to a company that, less than a year ago, hailed the virtues of simplification and focus. Where Global once insisted on concentrating its resources on SMBs, it now declaims: “there’s not a merchant from SMB to enterprise that we can’t serve”. Meanwhile, as far as I can tell, the cross-pollination of banking relationships, pitched as one of the chief synergies in the prior burst of mega-deals, had no discernable inflective impact on anyone’s growth prospects.

Legacy players chant “scale” like a hallowed incantation, as if size were the end all, regardless of how many regional platforms it was distributed across. And I’ll concede that decades ago legacy acquirers could get away with trumpeting cost synergies, neglecting product development, and forsaking the hard work of integrating acquired platforms. All sucked at innovation and platform integration together; all enjoyed close relationships with the banks and ISOs that controlled distribution. But that doesn’t cut it anymore. Stripe abstracted its payments apparatus behind a simple API that was rapidly adopted by developers; Adyen sold directly to e-commerce enterprises; Square terminals could be picked off the shelves of major retailers or ordered online. All prioritized easy onboarding and beautiful design, and eschewed the legacy model of scaling through transformative M&A, understanding that the easy wins (immediate scale, cost synergies) from such an approach could morph into an addiction that eventually concretizes into a millstone around the necks of those who succumb to it. In short, you can’t buy your way to relevance anymore. Global’s new CEO seemed to grok this too until, suddenly, he did not.

Conscious of the integration concerns inherent in a deal as enormous as Worldpay, management has recently been talking up a “a very, very small technology acquisition” that delivers “all of the same benefit of being on a single platform with a single database by having orchestration capabilities even at that middle tier that we’re operating sort of silently to the customers”. Geez, who knew that the colossal resources all these legacy acquirers have wasted over decades trying to integrate their fractured platforms could have been resolved with a single, inconsequential middleware acquisition. Checkmate, Adyen? C’mon now, hush on that noise.

IV.

In ripping on Global Payments, I hope I haven’t given the impression that the company trails behind it the ghastly remains of one failed acquisition after the next as it galumphs into irrelevance. Honestly, capital allocation hasn’t been that bad….far from great, but hardly ruinous. Yes, management was carried away by the post-COVID mania and paid ridiculous multiples for Zego (40x forward EBITDA) and MineralTree (15x forward revenue). (MineralTree, in particular, looks like a mistake in retrospect, its acquisition motivated by a now seemingly abandoned vision of combining its accounts payable automation service with TSYS’ commercial card and EVO’s receivables management capabilities to launch a B2B commerce organization that the former CEO, Jeff Sloan, hoped to 5x-10x over over five years through a land grab of M&A6).

Still, of greater consequence, the software-led distribution journey that management embarked upon more than a decade ago was directionally right and the low-teens EBITDA multiples paid for the heavy cluster of acquisitions in 2017-2018 were at least reasonable, even if the deal multiples were more a function of where valuations happened to be at the time than of rigorous valuation standards on management’s part (were the going rate more like 40x-50x EBITDA, I suspect Global would have reached). Notably, AdvancedMD, purchased for $700mn in 2018, was sold for a respectable $1.1bn (high-teens EBITDA multiple) last year. Even TSYS, though acquired for strategically dubious reasons, grew at by ~5%/year during Global’s ownership, which is about as much as one can ask for a legacy issuer processing asset. And while Global’s stock has lost more than half its value over the last five years and today trades 63% off of its 2021 peak, the SaaS craze is a rough starting point for a company that deliberately tried in both execution and messaging to position itself in the very eye of that hurricane7.

As you’ve no doubt gathered, I dislike the Worldpay acquisition. Global shareholders would be much better served by the focused agenda that management had in place prior to this year. But here we are! And God help me, for all the knocks against the company, the stock looks pretty damn cheap. On a standalone basis, Global trades at less 7x this year’s net earnings. The Worldpay transaction is expected to be accretive on day 1, so the stock is even cheaper than that on a pro-forma basis, even without taking into account the $600mn of cost synergies (18% of WP’s cost base). At the current price, an investor need not believe that Global will crash payments Olympus and claim a seat alongside Adyen and Stripe. Just that it won’t be snuffed out of existence. Humbly, I don’t think this is too difficult a bet to underwrite.

For all of its shortcomings, Global has a few things going for it.

First, it enjoys a huge software distribution footprint that includes tight relationships with ~3k ISV partners. Integrated and embedded payments make up just under half the company’s standalone revenue and are about as sticky as the software it’s woven into, with Integrated Payments clients retaining at a high-80s/low-90s rate and vertical software clients retaining at closer to 98%-99%.

Second, part of the software-led subsegment of Global’s merchant services segment comes from POS systems, which are now being consolidated and modernized under the Genius brand. It is right to be skeptical of Genius’ prospects, as Global has hardly demonstrated strong product sense over the years. But at least now, rather than simply dismissing Clover and Square as “Verifone replacements”, management is making a serious effort to compete. Genius will be a beneficiary of the $1bn/year (8% of PF revenue) that Global plans to spend developing products in the tech-forward portions of its portfolio.

Third, Global has the right kinds of distribution for Genius in the right places. In the US, distribution will be underpinned by a direct salesforce, acquired through Heartland, that traditionally sold legacy bricks in the mid/late-teens but has since been re-oriented around these growthier initiatives. Speaking to the importance of a direct salesforce, Shift4 has in recent years been acquiring ISOs in core markets. Internationally, bank partnerships are still important and far more relevant than they are in the US. And through its $4bn acquisition of EVO Payments in 2022, Global now finds itself the beneficiary of deep alliances with key banking partners in Germany, Greece, Poland, Spain, and Mexico.

Prior to the Worldpay deal announcement, management expected integrated and embedded revenue to grow high-single/low double-digit growth over the medium-term, up from high-single digits, as the transformation takes hold. “Core Payments”, which includes a variety of legacy products – among them, basic non-integrated shoebox terminals – distributed both directly and through traditional bank and ISO partners, represents 1/3 of Global’s standalone revenue and has been more like a mid-single digit grower, with double digit growth in international markets, comprising half of core payments, diluted by lsd growth in the US. This sub-segment is not a strategic priority for Global but at least gushes cash (high-40s margins) that can be reinvested in growthier stuff and potentially serves as a feeder for its modern payment services.

Worldpay, ~45% of pro-forma revenue, is growing mid-single digits, powered by hsd growth in e-commerce and enterprise, even as it continues to perennially donate share donor to Adyen. So if Worldpay is growing around 5% and standalone Global is tracking in the high-single digits, the combined entity’s organic growth should land somewhere around 6%-7%….though given the daunting integration challenges ahead and how unproven this behemoth is at product development, I wouldn’t be at all surprised to see growth come in several percentage points below that. But let’s say management’s guidance through 2027 pans out: topline expands msd/hsd and EPS grows by mid-teens through 100-200bps of annual margin expansion and aggressive buybacks/dividends ($6.8bn remaining through 2027, ~1/3 of the current market cap). In such a scenario, Global’s stock today trades at just 5x 2027 EPS and just 4x the $5bn of free cash flow that management thinks it can produce in 2028.

Let’s be clear: this is not a great company. But nor is it careering toward extinction, as the valuation would suggest. One can certainly understand why Elliott Management felt compelled to purchase shares in July, months after the Worldpay deal was announced and the stock tanked…and why I recently chose to roll in the mud with them too.

Disclosure: At the time this report was published, accounts I manage owned shares of GPN 0.00%↑ and FOUR 0.00%↑ . This may have changed at any time since

NDC provided data processing and information services across a number of verticals but, as card adoption surged during the ‘80s, payment processing emerged as its most profitable and strategically consequential. During the ‘90s, the company sold off its waning divisions and doubled down on payments and expanded its relationships with banks, for whom it operated as a back-end processor, authorizing and settling card transactions, and set up co-branded merchant acquiring joint ventures, where it played a more expansive role in supporting customers

ACTIVE Network – sports events, camps, class registrations; AdvancedMD – physician practice management, electronic health records, patient engagement; and SICOM – QSRs and fast-casual dining restaurants

the Cayan ($1.1bn) and Transfast ($2.4bn) the two most notable acquisitions

though FIS and Global have applauded Charles and GTCR for revitalizing Worldpay, the ex. synergy EBITDA for Worldpay disclosed through this transaction implies basically no growth since 2018

run-rate, net of reinvestment

at last disclosure in 2023, B2B was generating ~$125mn to $150mn of revenue and growing double-digit

though, in fairness, relative performance has been mediocre over a long stretch of time. Since Oct. 1, 2013, when Jeff Sloan took the reigns as and Global began prosecuting its software-first approach in earnest, the stock has returned just over 11%/year, underperforming the S&P 500 (~14%), Fiserv (~15.5%), Visa (~19%), and Mastercard (~20%), though happily outperforming the low bar set by FIS (~6.5%))

great read

Good to revisit this. Seems like adyen is the new adyen these days? Would love to read your thoughts on the drawdown