[LILAK – Liberty Latin America] Once more unto the breach

LILAK, the widow maker. For many years, a core holding of Generic Value Partners. This stock has been pitched many times, each new pitch underpinned by sensible-sounding premises that are by now so familiar that their recitation seems almost tiresome: cable moat, Malone, consolidation, forced selling, insider buying, secular growth. And yet, since it began trading as a tracking stock for the Latin American division of Liberty Global nearly 5 years ago, LILAK has lost nearly 80% of its value.

I don’t typically write about Liberty constituents because they are so comprehensively covered and universally loved (at least in the circles I roam), but LILA/LILAK have gotten so beat up that I just had to take my shot.

Back in 2014, buried under $8.4bn of EBITDA from Liberty Global’s European operations, were two fine but forgettable cable assets contributing $500mn of profits from small markets on a distant continent: VTR, the largest cable TV and internet provider in Chile, and Liberty Puerto Rico (LPR), the dominant cable and broadband provider in Puerto Rico, in which Liberty Global had a 60% stake1. Liberty Global took control of VTR in 2004, when Global’s predecessor’s predecessor, Liberty Media, acquired a majority stake in VTR’s parent, UnitedGlobalCom (UGC), a cable operator with mostly European operations2. Liberty PR, already the largest fixed line operator on the island following its 2012 acquisition of OneLink, advanced its leadership in 2015 by acquiring Choice Cable TV, the second largest cable and broadband service provider, growing its homes passed by 50% and extending its reach to over 80% of Puerto Rican homes.

Both VTR and LPR were chugging along just fine in 2014. VTR had been generating low-teens pre-tax returns, while growing revenue and profits at a mid/high-single digit annual rate over the prior 3 years. During the same period, LPR consolidated its foothold in Puerto Rico. But the company had ambitions to scale its presence across Latin America and wanted credit from the market as it did so.

So in July 2015, Liberty Global issued three classes of LiLAC tracking shares (LILA, LILAB, LILAK), 20 of each for every A, B, and C share respectively, of Liberty Global, intended to “track” the performance of Global’s Latin American and Caribbean operations (“LiLAC Group”). At the same time, the company issued Liberty Global tracking shares to track the performance of everything else3. Both series of tracking shares replaced “real” shares in Liberty Global, providing Liberty Global investors the flexibility to adjust their exposure to LiLAC (Latin America/Caribbean) and Liberty Global (Europe) as they pleased. In January 2018, LiLAC Group split off from Liberty Global, its tracking shares replaced one-for-one with shares of Liberty Latin America (LLA), a new entity containing all the operations, assets, and liabilities once attributed to LiLAC Group.

The fundamental business characteristics of cable are straightforward and well-known. Fixed costs and upfront investment are high while the costs of serving an incremental customer are low. Once acquired, customers are sticky since switching internet providers is inconvenient, especially when internet is purchased as part of a cable TV/mobile bundle. Absent meaningful product differentiation, a new entrant cannot easily gain the requisite share from incumbent players – who have lower average costs by virtue of having a relatively larger customer base over which to spread out their fixed costs – to justify the enormous upfront investment of laying and maintaining fiber. Thus, cable companies and other high fixed cost/low marginal cost businesses, like utilities, airlines, and semi fabs, tend towards oligopoly, making the cable/mobile industry in many of LLA’s markets far more crowded than it needs to be. Does Chile, a country with 5mn households, or Panama, a country with just 720k households, each need 4 mobile operators? Two (maybe 3) would probably suffice.

And so, management figured it would consolidate a fragmented telco landscape in Latin America and the Caribbean as it had successfully done in Europe (management thinks the consolidation opportunity in Latam/Caribbean is where Europe was 15 years ago), using LiLAC tracking shares as currency when sensible.

It got to work immediately. In November 2015, just 5 months after the tracking stocks were issued, Liberty Global announced the acquisition of Cable & Wireless, the #1 broadband provider in 11 of 15 Caribbean markets, and the #1 or #2 mobile operator in all 13 of its mobile markets. At around this time, CWC was in the middle of integrating Columbus International4, a Caribbean fiber-based telecom company that it had acquired earlier that year, to the great consternation of Digicel, a (primarily) mobile operator that competes with LiLAC in many markets. Digicel’s CEO fulminated against the Columbus merger, claiming it squashed the only real fixed line competitor to C&W in Jamaica, Trinidad & Tobago, Barbados, and several other territories, not to mention granted the combined entity control over the largest subsea fiber network in the Caribbean.

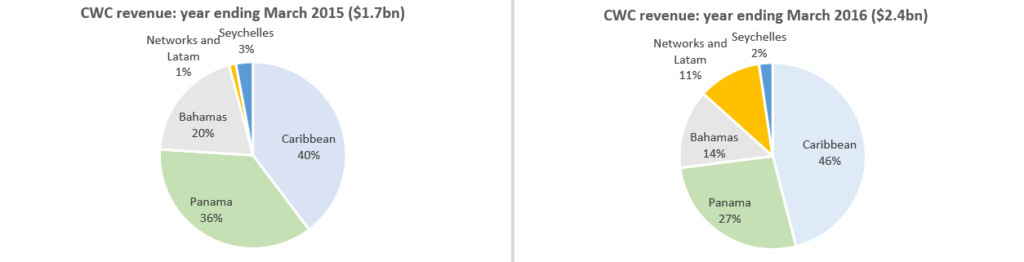

Here’s a snapshot of C&W’s revenue sources by geography before and after the Columbus acquisition…

…and here’s the before and after by product:

A few things. First, the Columbus acquisition propelled CWC to dominance in some products and bolstered its leadership in others, better positioning the combined company for “fixed/mobile convergence” (which basically just means bundling internet and cable TV with cell service). Second, it brought a promising new business segment – labeled “Networks and Latam” in the top right pie chart, lumped into “Other” in the lower right – that delivers broadband services to businesses and governments. And third, as a fiber-based telco, Columbus diluted the revenue contribution from mobile while expanding the contribution from video.

Although CWC was absorbed into LiLAC Group, Liberty Global acquired CWC mostly by issuing Liberty Global Group A and C tracking shares rather than LiLAC tracking shares, perhaps testament to how cheap management believed LiLAC’s stock was at ~$40/share, where it was trading at the time…but then puzzlingly, in June 2016, just a month after closing the CWC acquisition and with LiLAC shares value about where they were at the time of the CWC acquisition, the company announced that it would be issuing 117mn LiLAC shares to shareholders of Liberty Global Group, thus eliminating the latter’s interest in LiLAC Group, nearly quadrupling LiLAC’s share count, and prompting LILAK stock to sell off by more than 10%.

This was just the start. After management lowered full year 2016 guidance, LILAK plummeted by 25% in August, the decline perhaps exacerbated by selling from Liberty Global investors who inadvertently found themselves with Latam exposure when they mostly just wanted to own European cable. In November, after the company missed its own 3q growth expectations, the stock gapped down another 30%. So in late May 2015, just before the LiLAC share issuance was announced, LILAK was trading for $43. By Thanksgiving, it was at $19 and today it trades for $11. Oof!

There’s also the matter of whether CWC was worth the hefty share count dilution suffered by LiLAC shareholders. Management issued LiLAK shares valued at less than 8x OIBTDA to buy for 9.7x5 a telco whose business was heavily tilted to prepaid mobile; whose organic revenue growth had been flat-to-negative for years; and whose monopoly in the Bahamas was due to terminate later that year.