[RYAN] Ryan Specialty – the middlemen have middlemen

This is a companion piece to the Kinsale writeup from a few weeks ago, where I explained some of the key differences between admitted and non-admitted insurance. Basically, admitted insurance covers familiar risks with well-understood parameters that are underwritten in huge volume, like standard home and auto. Non-admitted (or “excess & surplus”) insurance addresses quirkier, irregularly-shaped risks – say, a nightclub with a shaky security record or a contractor doing hazardous exterior work in wildfire country. Admitted carriers who want to raise prices or change policy need approval from state regulators to do so. Non-admitted carriers do not. They can freely change prices and terms, add or remove exclusions, and negotiate bespoke coverage with clients.

Admitted and non-admitted insurance differ not only in the types of risks they cover and in the flexibility of underwriting, but also in how coverage is sourced and placed. In the admitted market, retail brokers, acting on behalf of insureds, typically go directly to standard carriers, like a Travelers or State Farm, to secure coverage. By contrast, the E&S market introduces an additional layer of intermediation, wholesale brokerage, that sits between retail brokers and carriers1. Wholesalers exist for two primary reasons:

1) Expertise: retail brokers tend to specialize by client and industry vertical. They know enough to guide clients through general liability, auto, workers’ comp, and other core coverages, but rarely possess deep expertise in every line, especially funkier stuff like certain cyber or employment practices liability, where coverage can hinge on highly nuanced policy language. So they turn to wholesalers who live and breathe those specialized exposures and understand which carriers or MGAs have appetite for which risks, at what price, and on what terms. Put another way, retail brokers tend to orient by client and industry (real estate, construction, healthcare) while wholesale brokers generally specialize by coverage type (cyber, directors & officers, environmental).

2) Carrier access: most retail brokers cannot deliver enough volume in a given niche exposure to justify a direct relationship with E&S carriers, who generally do not want to manage thousands of small distribution relationships. Many carriers prefer – and some effectively require – that business flow through wholesalers, who can aggregate submissions from a broad network of retailers. Large retail brokers like Aon and Marsh can often place business directly, but even they still rely wholesalers for oddball risks that fall outside core carrier relationships.

For example, imagine a retail broker representing the owner of a large apartment complex. The broker can comfortably place standard coverages like property, general liability, workers’ compensation, and umbrella, but may be less equipped to source coverage for a more specialized exposure, such as pollution liability tied to mold or asbestos. In that case, the broker would turn to a wholesaler with expertise in environmental lines, who would then approach the E&S carriers it knows have appetite for that risk, gather quotes and proposed terms, and help the retail broker evaluate the trade-offs among them. The carrier pays ~15%-20% of premiums as a fee to the wholesaler and the wholesaler in turn pays ~10% of that to the retailer, keeping ~5%-10% for itself.

In the flow I’ve described – client → retail broker → wholesale broker → carrier – the wholesaler places risk, but isn’t involved in any underwriting decisions. But there are other entities in the E&S ecosystem who are. They go by different names and have somewhat different responsibilities, but what they share in common is broad authority, granted to them by an insurance carrier, to underwrite and bind coverage.

Managing general agents (MGAs, or managing general underwriters, MGUs) design specialized coverage for complex or awkward classes of risk that standard carriers often avoid…higher-hazard retail businesses like liquor stores, cannabis dispensaries, and nightclubs; specialty contractors like as roofers and scaffolders; and habitational risks like older apartment complexes or coastal mobile-home communities. Many present themselves as product-line specialists for specific industries. Ryan’s stable includes MGUs that cover niche risks like post-harvest agriculture property (Agrisk Underwriters); amusement, entertainment, and leisure industries (Alive Risk), and commercial auto for hazmat trucking operations (Freberg Environmental).

Program managers are another subset of the broader delegated-authority world. Like MGAs, they operate under the authority granted to them by carrier partners. But whereas MGAs primarily execute underwriting and binding within a carrier’s existing framework, program managers function more like product owners in that they also design the coverage offering, develop underwriting rules and rating logic, coordinate reinsurance, and otherwise oversee the day-to-day operations of a cohesive program built for a narrowly defined niche (from here on out, I’m going to refer to all delegated underwriters as MGAs. Just keep in mind that this includes different flavors, like program managers).

One reason E&S carriers outsource underwriting and binding authority to MGAs in the first place is that MGAs are often entrepreneurial specialists that build deep expertise in narrow pockets of risk that are not worth the resources for a carrier to develop internally. In the cannabis industry, for instance, dispensaries may have unique cash handling and security protocols while processing facilities may introduce unique fire and explosion hazards, with ventilation and suppression standards that vary by state. It is often faster and more efficient for carriers to access such risks through MGAs than to invest behind the infrastructure to do so themselves.

Another, more structural consideration is that carriers are limited by portfolio management considerations, which might prohibit further exposure to, say, roofers in a wildfire-prone region. An MGA, by contrast, is less constrained by its own balance sheet and can continue underwriting that business so long as it can place the risk with carrier partners that still have appetite and capacity for it.

MGAs and wholesale brokers play complementary roles in the E&S ecosystem. A wholesaler’s job is to place risk sent to them by retailers and sometimes those risks are so niche that, absent MGAs who specialize in underwriting them, they might never be placed at all. At a high level, then, MGAs function like distributors from the insurer’s perspective but look more like underwriters from the wholesaler’s.

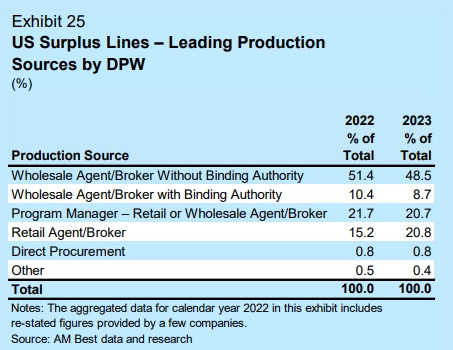

From the point of view of US E&S insurers, direct premiums break down roughly as follows:

Only ~20% of E&S premiums are directly placed by retail brokers. Nearly of the other ~80% is intermediated through MGAs and wholesalers with and without binding authority.