[scuttlebit] Danaher update

It’s been nearly three years since I last wrote up Danaher and Thermo Fisher, so I figure it’s time for an update, especially with both companies announcing huge acquisitions recently.

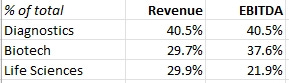

Let’s start with Danaher, specifically its Diagnostics division, which sells instruments and associated consumables that hospitals use to diagnose diseases. Though accounting for 41% of revenue and EBITDA, it seems to draw far less attention than Danaher’s two, relatively smaller segments.

And I get it. Unlike Life Sciences, the locus of recent M&A, Diagnostics has been starved of acquisitions for the better part of a decade. And compared to Bioprocessing, it competes in a far more crowded arena, with formidable rivals across multiple testing categories, and enjoys weaker regulatory and process-validation lock-in.

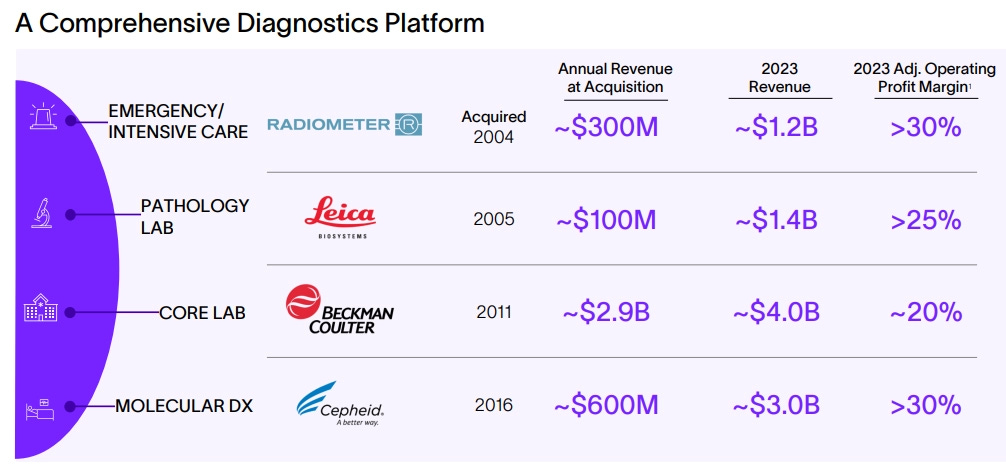

But Diagnostics is also where Danaher’s vaunted kaizen values of continuous improvement, codified as the Danaher Business System, has arguably made its biggest mark on acquired targets. I mean, they’ve crushed it here:

(for reference: Radiometer manufactures blood gas analyzers that provide ICU and emergency room physicians with rapid measurements of oxygen, carbon dioxide, pH, and electrolyte levels in the blood to determine whether a patient’s lungs, circulation, and metabolism are functioning as they’re supposed to.

Leica Biosystems sits in the pathology workflow, its instruments and reagents used by oncologists to check for cancer in tissue samples collected in biopsies or during surgery.

Beckman Coulter is the backbone of “core labs”, providing products for routine blood and urine tests that are run in huge volumes.

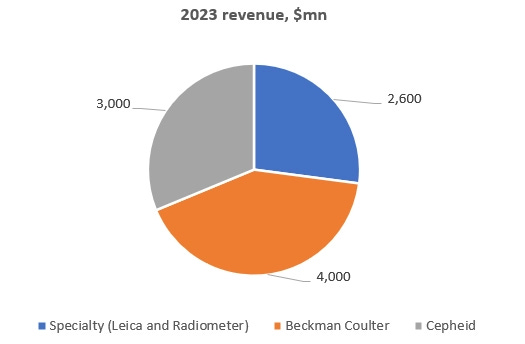

Cepheid specializes in molecular diagnostics, particularly PCR testing through its GeneXpert platform. Its products are used to identify the genetic signatures – DNA, RNA – of pathogens responsible for diseases like tuberculosis, COVID-19, flu, and MRSA. See below the relative revenue contributions in 2023; I don’t think these have materially changed in the past two years)

Danaher’s 2024 Analyst Day gets into the gory details. Specialty Diagnostics (Radiometer + Leica) has grown revenue by hsd in the decade from 2013 to 20231 and generates returns on invested capital of more than 20%.

Beckman Coulter went from no revenue growth and paltry 12% EBITA margins to now growing msd+ (ex. China), with ~20% EBITDA margins and dd+ ROICs. By 2023, it generated twice as much new product revenue as it did 2018, having introduced more automation for lower-volume small and mid-sized labs and narrowed the menu gap to Roche and Abbott with assays for bloodborne viruses like HIV and hepatitis, as well as cardiac biomarkers linked to heart failure2.

Notwithstanding these gains, it’s fair to say that Beckman Coulter is a mustier asset than some of Danaher’s other diagnostic brands. Cepheid, for instance, enjoys a far stronger reputation in molecular diagnostics than Beckman does in routine lab diagnostics, a category that has become increasingly commoditized over time.