Simulation, CAD, and PLM: Part 1

Many of the complex objects and structures around you were conceived as virtual objects modeled in computer-aided design (CAD) software. Those CAD objects may have been converted into millions of small polygons (pre-processing), each one bombarded with advanced calculus to help engineers visualize the polygonal mesh’s response to different simulated physical conditions (post-processing).

Simulation tools codify physical laws into software so that engineers can see how a product fares under real world stresses. Whereas you will often see CAD and industrial automation companies specialize by sector – Autodesk is big in architecture, engineering, and construction (AEC); PTC focuses on manufacturing; Dassault, Siemens, and Hexagon organize their solutions by industry groups – simulation players, because they model universally applicable physics, cover a broad range of industries in a more generic way.

So, using compute-aided engineering (CAE) tools (from now on, I will use “simulation” and “CAE” interchangeably), an engineer might visualize airflow as it passes through different windmill designs at different wind speeds; model the interaction of various hip socket sizes and shapes with bone material; simulate the stress on steel I-beams with different yield strengths1 under varying loads at different temperatures and the performance of 5G chips at very high frequencies; assess the structural response of a smartphone, airplane or reinforced concrete beam to different impact velocities (i.e. what happens to your smartphone when it falls from 2 meters or an airplane when it runs into a bird or a bridge when stomped on by Godzilla?). As part of its jet engine testing, Rolls Royce draws on Ansys’ library of properties (tensile strength, thermal conductivity, heat capacity, etc.) on 700 different metals, plastics, and other materials.

Compared to building and testing a physical model, virtual simulation can shave weeks or months off product development and allows engineers across all kinds of industries, from automotive to aerospace, to identify design errors early in the product’s lifecycle, when they can be easily fixed. The decisions made during the design and sketch phase of product development have massive consequences. You don’t want an implanted artificial hip socket to unexpectedly fold under stress or an aerospace alloy to melt mid-flight…probably better to have that stuff happen inside a software simulation. Also, it’s much less expensive and time consuming to develop different design configurations in software than it is to construct physical models, which allows for more experimentation.

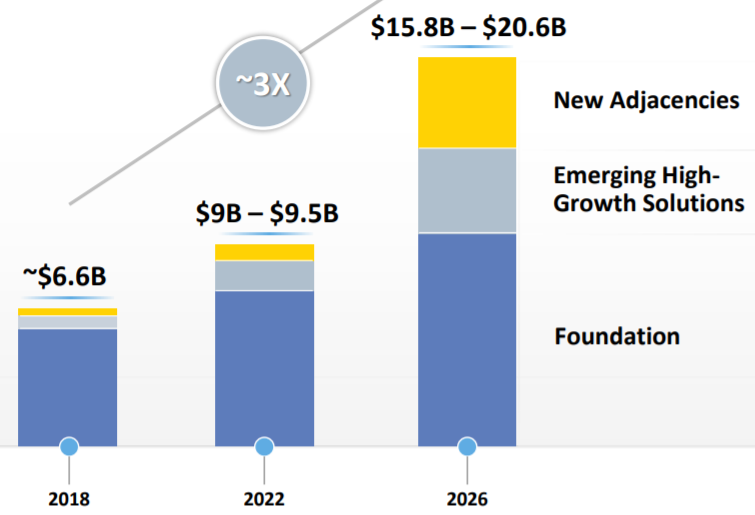

Here is the market opportunity, according to Ansys:

The blue “Foundation” bar in the above chart, which refers to core design and ideation use cases, is growing by ~9%/year. The grey part of the bar chart, growing by 20%/year, is just an extension of the core blue part and refers to frontier stuff like 5G chips, drones, and electric and autonomous vehicles. In recent years, Ansys has acquired capabilities in optical (OPTIS), radar (HFSS), and electromagnetic simulation (Helic), which are being combined with existing tools in fluids, electronics, and materials to develop simulation stacks for these applications.

Simulation tools have been around since at least the 70s, and today are used by every company that could need them, but the market keeps growing because 1/ mounting product complexity demands more advanced tooling; and 2/ advances in computing power/cost and technology reduce the cost of running compute-taxing simulations and expand simulation use cases. Investors worried about saturation as far back as the early 2000s, and yet 20 years later the industry continues to grow at a high-single digit pace.

With software and electronics components increasing their product footprints, component level analysis evolving towards system level simulations, where interactions between myriad parts of a system are modeled against the backdrop of several simultaneous physical processes (“multi-physics”). As part of this evolution, Ansys began directly upselling more “physics” into the heavy R&D spenders with whom it forged long-term collaborative relationships, pushing enterprise license agreements that consolidated all the key tools on a single platform.