S&P, Moody’s, and the limits of AI disruption: Part 1

(Part 1 concerns S&P Global; Part 2 will be published next week and discusses Moody’s)

Moody’s and S&P Global have this year traded as a blended average of two different businesses: a deeply moated ratings franchise that is largely insulated from AI disruption, and a data and analytics operation that is squarely in its crosshairs. In the current AI panic, each stock has sold off roughly in proportion to its exposure to the latter.

I don’t think anyone is confused about what makes credit ratings a GOAT business. But just in case, here’s what I wrote about it back in 2017:

…ratings underpin the risk weightings that banks attach to assets to determine capital requirements, dictate which securities a money market fund can own, and, in ostensibly surfacing the credit risk embedded in fixed income securities, make it easier for two parties to confidently price and trade, enhancing market liquidity.

Because of such industry-wide adoption, a debt issuer has little choice but to pay Moody’s for a rating if it hopes to get a fair deal in the market: an issuer of $500mn in 10-year bonds might pay the company 6bps ($300k) upfront, but will save 30bps in interest expense every year ($15mn over the life of the bond)….and each incremental issuer who pays the toll only further reinforces the Moody’s ratings as the standard upon which to coalesce, fostering still further participation. This feedback loop naturally evolves into a deeply entrenched oligopoly.

Moody’s and S&P enjoy what I described back then as a “standards moat”. The durability of their credit ratings have less to do with the relative accuracy of default and loss assessments than by the role they play as a ubiquitously adopted benchmark across the financial ecosystem. A startup could conceivably use AI-powered algorithms to create a ratings methodology that was just as accurate and Moody’s and S&P’s would still remain entrenched.

A similar logic holds for S&P’s equity index business. From [SPGI, MCO] Market infrastructure: part 2:

Likewise, the utility of equity indices like the Russell 2000, FTSE 100, S&P 500, and The Dow Jones, is derived from consensus rather than from absolute standards of reasonableness. The Dow Jones Index methodology, which weights its 30 constituents by share price, is routinely mocked as non-sensical, but its absurdity is more feature than bug as it suggests that a more sensible index couldn’t just come along and displace it the same way that a better technology might, in theory, replace entrenched network effects.

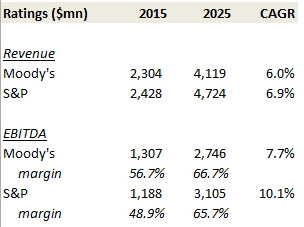

The credit ratings business should be buoyed by several durable growth themes over the foreseeable future. Some $5tn of debt needs to be refinanced over the next four years, roughly double the dollar volume seen in 2018. The swelling stock of private credit will increasingly demand risk scores too, as regulators and investors press for comparability with public debt markets; Moody’s private credit ratings revenue grew 60% last year. Infrastructure funding, including AI data centers, supplies a further tailwind. Ratings revenue is lumpy and unpredictable year to year, but over extended periods has reliably tracked the high-single digit growth rate that management has long guided to. I don’t expect the future to look much different from the past.

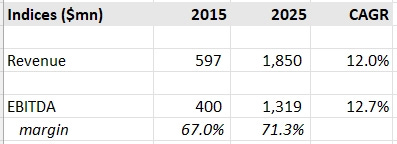

S&P’s Indices segment, meanwhile, should continue to be fueled by market appreciation and the same two secular tailwinds – active-to-passive migration and thematic benchmark creation – that have powered double-digit revenue growth over the past decade, with a potential third growth kicker emerging in the form of private market index products.

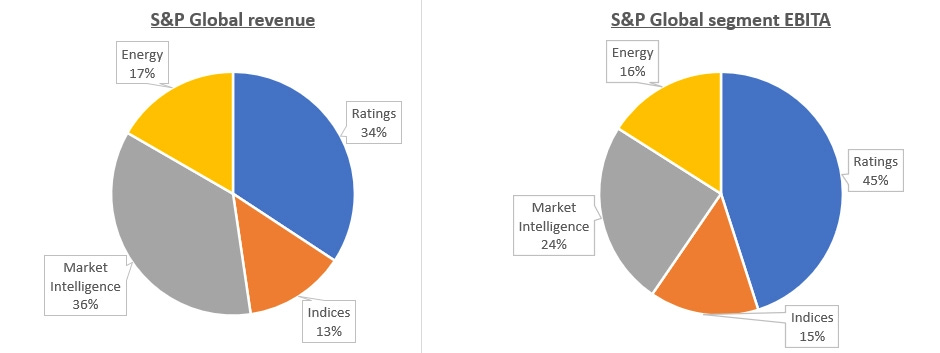

Excluding the soon-to-be spun off Mobility segment, Ratings and Indices1 together account for ~60% of segment-level EBITA. The remaining 40% is split across Market Intelligence and Energy. The latter two segments are a mishmash of data and analytics, and both were dramatically enlarged through the $44bn acquisition (~26x EBITDA) of IHS in 2022 (for more, see my March 2021 writeup: Thoughts on the S&P Global / IHS Markit merger):

Market Intelligence is a portfolio of products that management divides into three subsegments. The first and largest is Capital IQ, which provides financial and market data – including deep sector-specific data related to banking, insurance, real estate, and utilities, picked up through the $2bn acquisition of SNL – that investment professionals and sell-side analysts use to research companies, build valuation models, check estimates, and track markets, either by logging into a dedicated Bloomberg-like terminal or by piping it directly into their own systems.

The second is Enterprise Solutions, software that banks and asset managers use to manage loan portfolios (Wall Street Office), monitor private company holdings (iLEVEL), and manage the process of structuring and trading syndicated loans (ClearPar and Debtdomain).

Credit & Risk Solutions, the third subsegment of Market Intelligence, commercializes research and data related to S&P’s credit ratings, and offers tools that measure credit risk and analyze how sensitive a portfolio or company is to changes in credit conditions. It think about C&RS as S&P’s way of double dipping on its dominant ratings franchise. S&P realizes revenue once by issuing a bond rating, and then again by selling detailed research reports justifying the rating to banks, insurers, asset managers, and corporate treasury teams who buy those bonds.

S&P’s Energy segment combines Platts and IHS Resources, and serves energy producers, refiners, utilities, trading firms, brokers, and basically any commercial entity that traffics in commodities. It publishes thousands of daily benchmark prices – across oil, fuels, gas, chemicals, food and other commodities – that are ubiquitously referenced in contracts and used to settle trades. It also sells news and analytics to explain supply and demand trends, and offers data and software that drillers use to find promising oil fields and estimate how productive those fields might be.

In response to investor fears over AI, S&P released this helpful exhibit, which I’m going to use as a prompt for thinking about where the company is most and least exposed: