S&P, Moody’s, and the limits of AI disruption: Part 2

I briefly discussed credit ratings in my S&P write-up. It’s a great business, we all know that. But it’s also tied to issuance volume, which is highly cyclical and difficult to predict. Investors tend to dislike that kind of volatility even in deeply moated companies. Perhaps in an effort to smooth its earnings profile through long-term contracts and recurring revenue, Moody’s diversified away from the ratings franchise with the launch of a data and analytics segment in 2008, which has been bulked up through a number of significant acquisitions over the years.

But as with the non-ratings and non-index parts of S&P, Moody’s Analytics has also come under scrutiny as a business vulnerable to AI disruption. Moody’s Investor Service, the ratings division of the company, accounts for 70% of total profits. But that still leaves 30% AI-exposed, so investors are concerned.

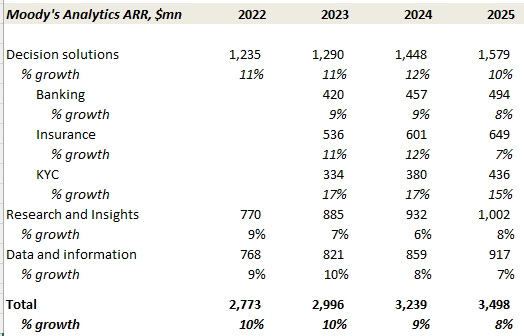

Moody’s Analytics is composed of three sub-segments: Decision Solutions, Research & Insights, and Data & Information:

In my S&P write-up, I explained:

Credit & Risk Solutions, the third subsegment of Market Intelligence, commercializes research and data related to S&P’s credit ratings, and provides tools to measure credit risk and analyze how sensitive a portfolio or company is to changes in credit conditions. It think about C&RS as S&P’s way of double dipping on its dominant ratings franchise. It realizes revenue once by issuing a bond rating, and again by selling detailed research reports justifying the ratings to banks, insurers, asset managers, and corporate treasury teams who invest in those rated bonds.

Research & Insights is the Moody’s equivalent. It monetizes the content that MIS generates in the producing credit ratings. Around 2/3 of its revenue comes from research reports that analysts write on rated companies, the remainder from credit scoring tools that clients use to spot credit deterioration, dig into the drivers of credit risk, and run scenario analyses.